HRT 374 Lecture Notes - Lecture 5: Seating Capacity, Current Liability, Deferral

29 Feb 2020

School

Department

Course

Professor

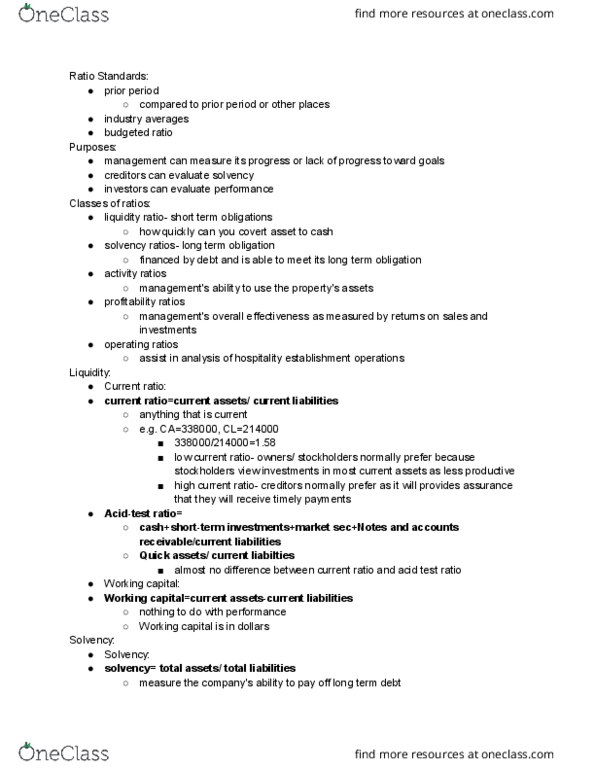

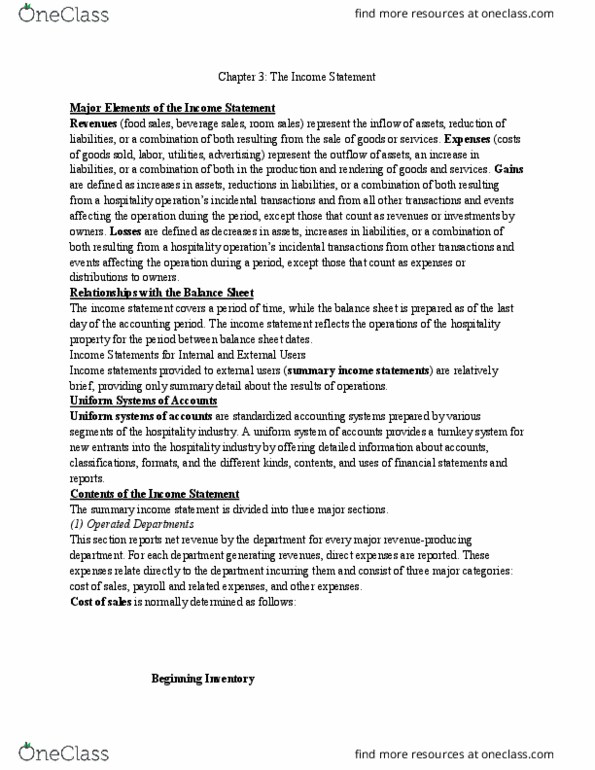

Chapter 5 - Ratio Analysis

Ratio Standards

Ratio analysis is used to evaluate the favorableness or unfavorableness of various financial

conditions. There are three different standards that are used to evaluate the ratios computed for a

given operation for a given period: ratios from a past period, industry averages, and budged

ratios.

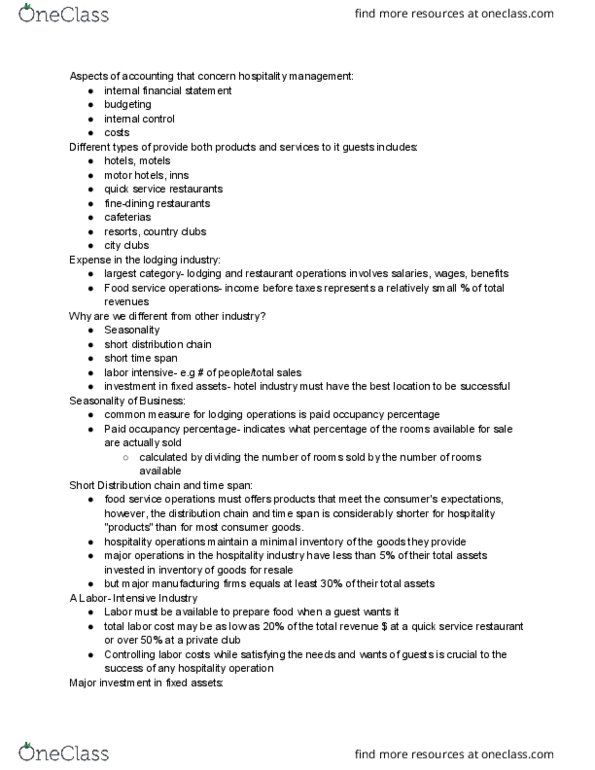

Purposes of Ratio Analysis

Ratios help managers monitor the operating performances of their operations and evaluate their

success in meeting a variety of goals.

What Ratios Express

Ratios are read in different ways:

Percentages - express the cost of food sold in terms of a percentage of total food sales. If total

food sales for a given year are $430,000, while the cost of food sold is $135,000, then the result

of dividing the cost of food sold by the total food sales is .314. Because the food cost percentage

is a ratio expressed as a percentage, this figure is multiplied by 100 to yield a 31.4 percent food

cost.

Per Unit Basis - For example, the average breakfast check is a ratio expressed as a certain sum

per breakfast served. It is calculated by dividing the total breakfast sales by the number of guests

served during the breakfast period. Thus, on a given day, if 100 guests were served breakfast and

the total revenue during the breakfast period amounted to $490, then the average breakfast check

would be $4.90 per meal ($490 ÷ 100).

Turnover - determined by dividing the number of guests served during a given period by the

number of restaurant seats. If the restaurant in the previous example had a seating capacity of 40

seats, then seat turnover for the breakfast period in which it served 100 guests would be 2.5 (100

÷ 40). This means that, during that breakfast period, the restaurant used its entire seating capacity

2.5 times

Coverage - For example, if a hospitality operation reported current assets of $120,000 and

current liabilities of $100,000 for a given period, then the operation’s current ratio at the balance

sheet date would be 1.2 to 1 (120,000 ÷ 100,000). This means that the hospitality operation

possessed sufficient current assets to cover its current liabilities 1.2 times. Put another way, for

every $1 of current liabilities, the operation had $1.20 of current assets.

Classes of Ratios

(1) Liquidity

Liquidity ratios reveal the ability of a hospitality establishment to meet its short-term

obligations

(2) Solvency

Solvency ratios measure the extent to which the enterprise has been financed by debt and is able

to meet its long-term obligations

(3) Activity