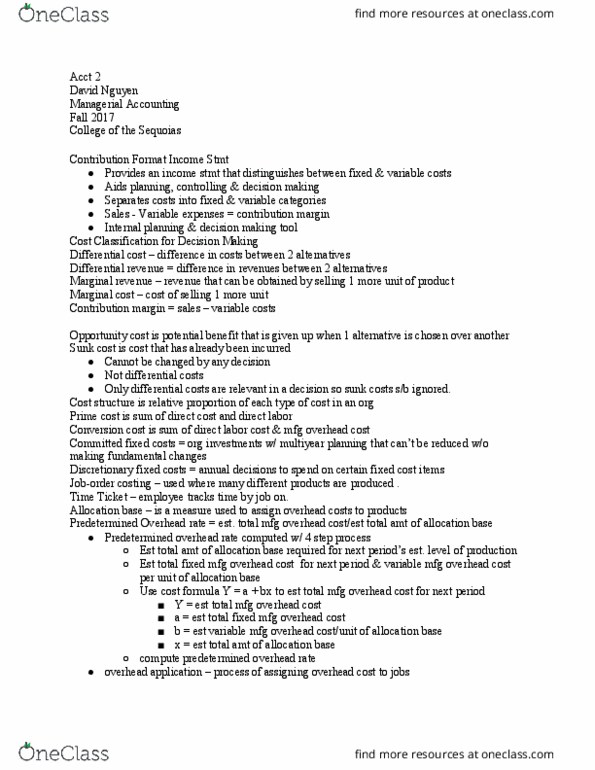

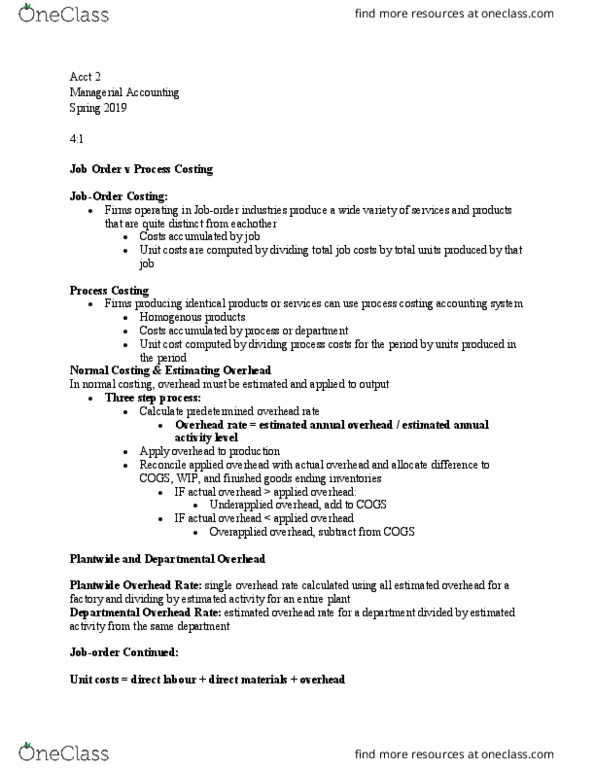

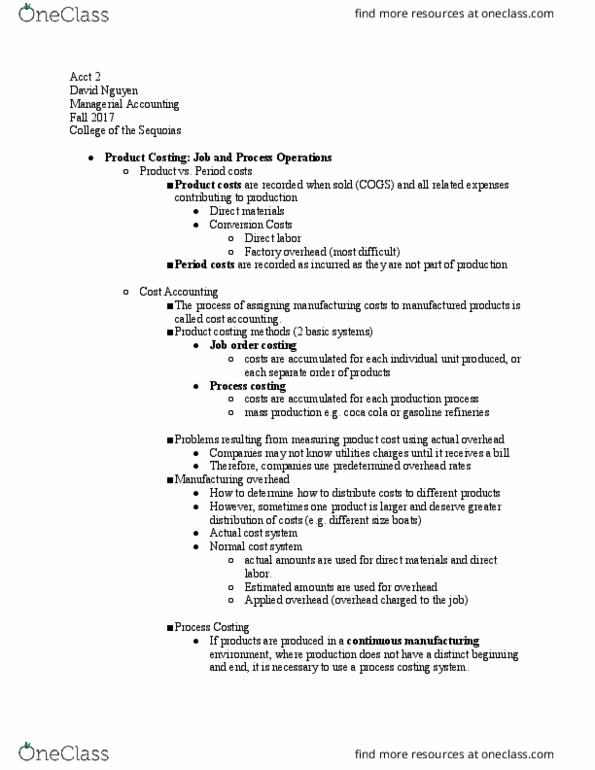

Valport Company, a manufacturer of fiber optic communications equipment, uses a job-order costing system. Since the production process is heavily automated, manufacturing overhead is allocated on the basis of machine hours using a predetermined overhead rate. The current annual rate of $15 per machine hour is based on budgeted manufacturing overhead costs of $1,200,000 and a budgeted activity level of 80,000 machine hours. Operations for year 20xx have been completed, and all of the accounting entries have been made for the year except the allocation of manufacturing overhead to the jobs worked on during December, the transfer of costs from Work in Process to Finished Goods for the jobs completed in December, and the transfer of costs from Finished Goods to Cost of Goods Sold for the jobs that have been sold during December. Summarized data as of November 30, 20xx and for December 20xx are presented in the following table. Jobs T11-007, N11-013, and N11-015 were completed during December. All completed jobs except Job N11-013 had been turned over to customers by the close of business on December 31, 20xx.

Work-in-Process December 20xx Activity

Balance Direct Direct Machine

Job No. 11/30/xx Material Labor Hours

T11-007 $ 87,000 $ 1,500 . $ 4,500 300

N11-013 55,000 4,000 12,000 1,000

N11-015 -0- 25,600 26,700 1,400

D12-002 -0- 37,900 20,000 2,500

D12-00 . -0- 26,000 16,800 800

________ _______ ______ _______

Total $142,000 $95,000 $80,000 6,000

Activity December

through 20xx

11/30/xx Activity

Actual manufacturing overhead incurred:

Indirect material . . . . . . . . . . . . . . . . . . . . . . . . $125,000 . . . . . . . . $ 9,000

Indirect labor. . . . . . . . . . . . . . . . . . . . . . . . . . . 345,000 . . . . . . . . 30,000

Utilities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245,000 . . . . . . . . 22,000

Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . 385,000 . . . . . . . . 35,000

Total overhead . . . . . . . . . . . . . . . . . . . . . . . . . $1,100,000 . . . . . . . $96,000

Other items:

Raw-material purchases* . . . . . . . . . . . . . . . . . $ 965,000 . . . . . . . $98,000

Direct-labor costs . . . . . . . . . . . . . . . . . . . . . . $ 845,000 . . . . . . . . 80,000

Machine hours . . . . . . . . . . . . . . . . . . . . . . . . . 73,000 . . . . . . . . 6,000

Account Balances at Beginning of Year 1/1/xx

Raw-materials inventory* . . . . . . . . . . . . . . . . . . . . $105,000

Work-in-process inventory . . . . . . . . . . . . . . . . . . . 60,000

Finished-goods inventory . . . . . . . . . . . . . . . . . . . 125,000

*Raw-material purchases and raw-materials inventory consist of both direct and indirect materials. The balance of the Raw-Materials Inventory account as of December 31, 20xx is $85,000.

REQUIRED:

How much manufacturing overhead would Valport have allocated to jobs through November 30, 20xx?

How much manufacturing overhead would be allocated to jobs by Valport during December 20xx?

Determine the amount by which the manufacturing overhead is overallocated or underallocated as of December 31, 20xx?

Determine the balance in Valport Company's Finished-Goods Inventory account on December 31, 20xx? (Hint: which completed job(s) are still in the finished goods warehouse as of December 31, 20xx?)

Determine the balance in Valport Company's Work-in-process Inventory account on December 31, 20xx? (Hint: which incomplete job(s) are still in the factory as of December 31, 20xx?)

Prepare a Schedule of Cost of Goods Manufactured for Valport Company for the year 20xx. (Hint: In computing the cost of direct material used, remember that Valport includes both direct and indirect material in its Raw-Materials Inventory account i.e.

Raw materials used in 20xx = Direct materials used in 20xx + Indirect materials used in 20xx)