ACCT 002 Lecture 21: Acc 2 11_1

5 Aug 2020

School

Department

Course

Professor

Document Summary

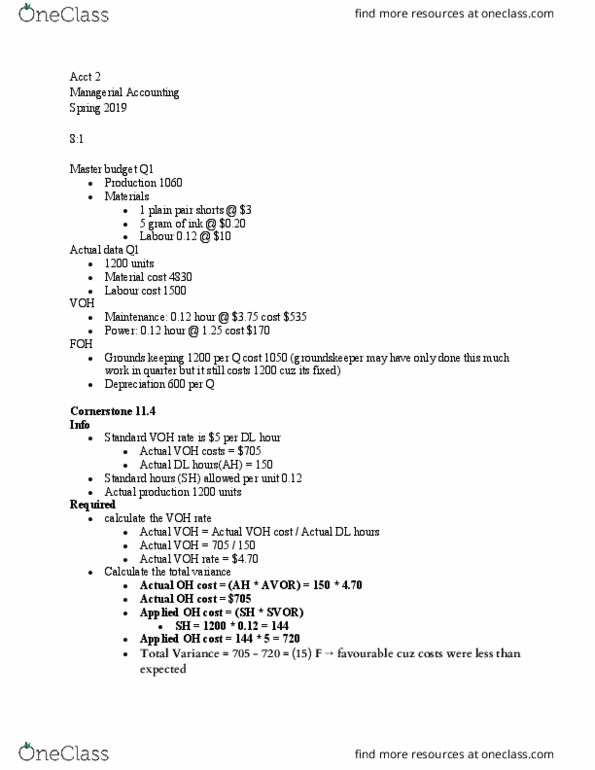

11:1 materials and it should reflect the final, delivered cost of those materials produce one unit of finished goods. Direct labor quantity and price standards are usually expressed in terms of labor hours or a labor rate for each unit of finished product, including an allowance for normal inefficiencies such as scrap and spoilage. Standard quantity per unit- defines the amount of direct materials that should be used. Standard price per unit- defines the price that should be paid for each unit of direct. Standard hours per unit- defines the amount of direct labor hours that should be used to. Standard rate per hour- defines the company"s expected direct labor wage rate per hour, *the standard rate per unit that a company expects to pay for variable overhead equals. Standard cost card- shows the standard quantity (or hours) and the standard price (or. Flexible budget performance report for variable manufacturing costs.