ACC 117 Lecture Notes - Lecture 27: Income Statement, Fixed Cost, Indian Railways

Charlie Kent

ACC 117

Summer 2017

Introduction to Anthropology

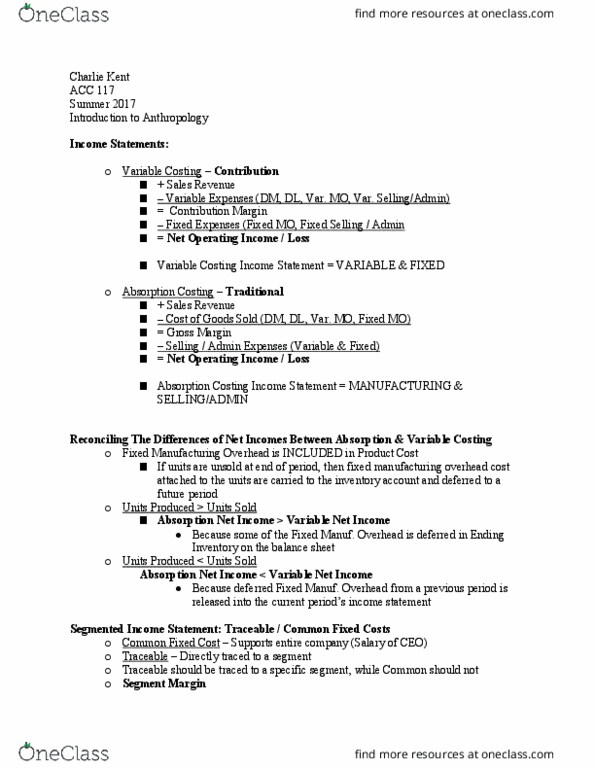

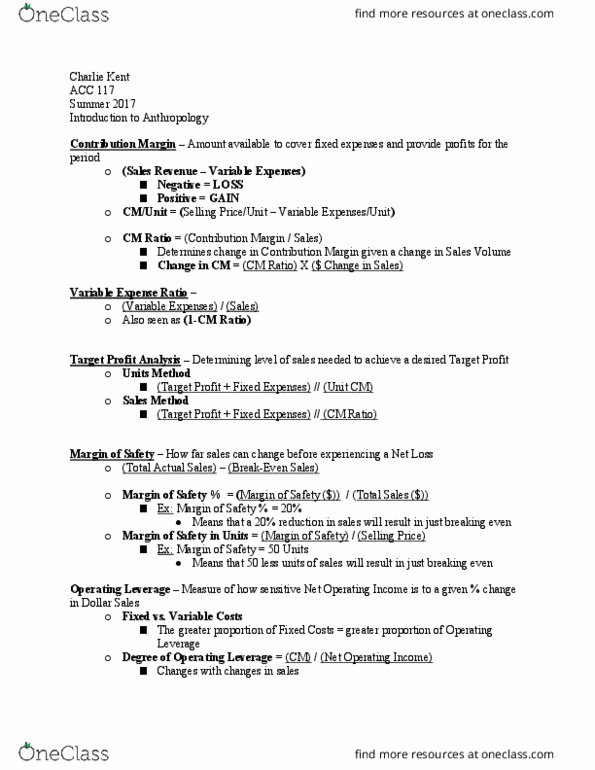

● Calculating Contribution Margin

○ Unit

○ Ratio

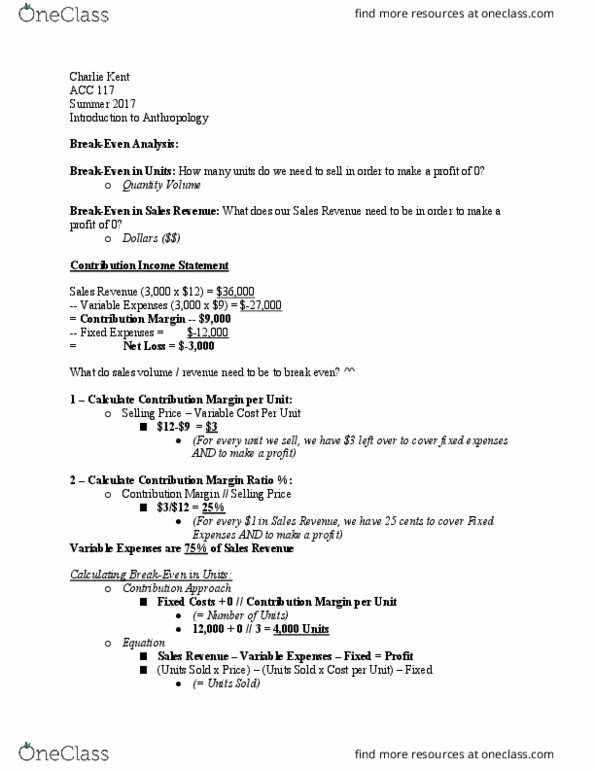

Break Even in Units & Sales

○ Profit = 0

○ Common AND Traceable Fixed Costs (All Fixed Costs)

Margin of Safety

Calculating Degree of Operating Leverage

○ How sensitive company’s net income is to changes in sales

Absorption Costing

○ Cost/Unit

○ Income Statement

○ Net Income

Variable Costing

○ Cost/Unit

○ Income Statement

○ Net Income

Segment Reporting

○ Breaking down Income Statement by Project / Section

■ Break-Even by Segments (Traceable Fixed Costs)

Activity-Based Costing

○ Rates

○ Allocate Overhead (Rate x Actual Activity)

○ Allocate to either a Job or Customer

○ Customer Margin (same thing as Customer Profit)

■ Sales for the customer – All the costs for the customer

Profit Planning –

○ Accomplished by a collection of Budgets (Master Budget)

Budget – Detailed plan for the future

○ Planning

■ Developing goals

Document Summary

Common and traceable fixed costs (all fixed costs) How sensitive company"s net income is to changes in sales. Breaking down income statement by project / section. Allocate to either a job or customer. Customer margin (same thing as customer profit) Sales for the customer all the costs for the customer. Accomplished by a collection of budgets (master budget) Monitoring, to ensure proper execution of plans. Help communicate plans and motivate managers to plan for future. System of accountability in which managers are held responsible over items of revenue and cost over which they have significant control. Most are usually 1 year fiscal year of the company. Requires review and re-appraisal throughout the year. Continuous budgets 12 months, and 1 month is added after the end of each month (ex) Self-imposed budget prepared with full participation and awareness of managers at all levels. Acceptance and how budget data is used by people in key positions.