ACC 250 Lecture Notes - Lecture 12: Current Asset

10 Jun 2018

School

Department

Course

Professor

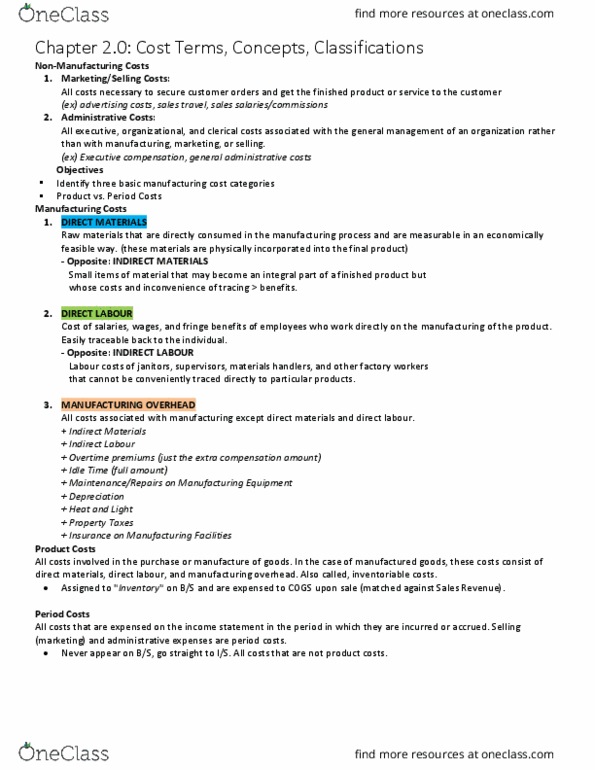

Factory overhead includes a range of expenses that support the manufacturing process. These

include indirect labou, which is different than direct labour. Indirect labour represents wages

to workers who support the manufacturing process.

Together, raw materials used, direct labour, and factory overhead represent the

manufacturing costs for fiscal period. Howeve, you must remember that on any given day,

including the start and end dates of a fiscal period, there is bound to be unfinished work in the

factory. This is called goods in process. Goods in process refers to goods that have had some

raw materials, direct labour, or overhead applied to them, but that are not yet in their finished

states.

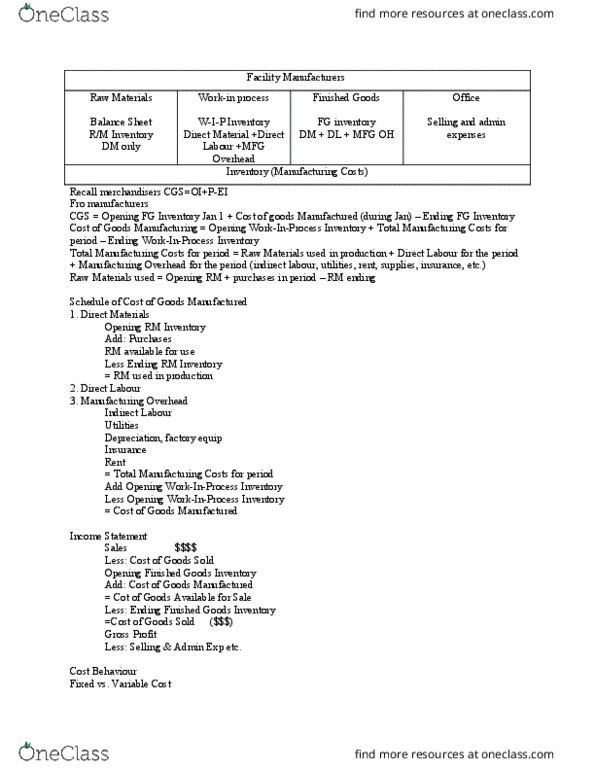

To arrive at an amount for the cost of goods manufactured, you must include work in process.

Therefore, add the total manufacturing costs to the value of goods in process at the beginning

of the year. The answer represents the total goods in process for the year. When you deduct

the value of goods still in process at the end of the year, the difference must be the value of

finished or manufactured goods.

Comparing Balance Sheets

In the current asset section of the merchandising firm, you will find an account named

merchandise inventory. This represents the cost value of merchandise on hand. In contrast,

the manufacturing business lists three inventory accounts in its current asset section. The first

is finished goods inventory, which is comparable to merchandise inventory.

Due to the complexities of manufacturing accounting, some educational institutions delay its

introductions until students reach their second year of post secondary studies. Yet, by being

exposed to manufacturing accounting at this time, you benefit in at least two ways. First, you

can see how a sound knowledge of merchandise accounting and the cost of goods sold

formula can help you understand manufacturing statements. And second, by recognizing the

great variety of costs associated with manufacturing a good, you can begin to appreciate the

important role of a cost accountant.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Factory overhead includes a range of expenses that support the manufacturing process. These include indirect labou, which is different than direct labour. Indirect labour represents wages to workers who support the manufacturing process. Together, raw materials used, direct labour, and factory overhead represent the manufacturing costs for fiscal period. Howeve, you must remember that on any given day, including the start and end dates of a fiscal period, there is bound to be unfinished work in the factory. Goods in process refers to goods that have had some raw materials, direct labour, or overhead applied to them, but that are not yet in their finished states. To arrive at an amount for the cost of goods manufactured, you must include work in process. Therefore, add the total manufacturing costs to the value of goods in process at the beginning of the year. The answer represents the total goods in process for the year.