SMG SM 131 Lecture Notes - Lecture 2: Financial Statement, Retained Earnings, Trial Balance

12 Sep 2018

School

Department

Course

Professor

Document Summary

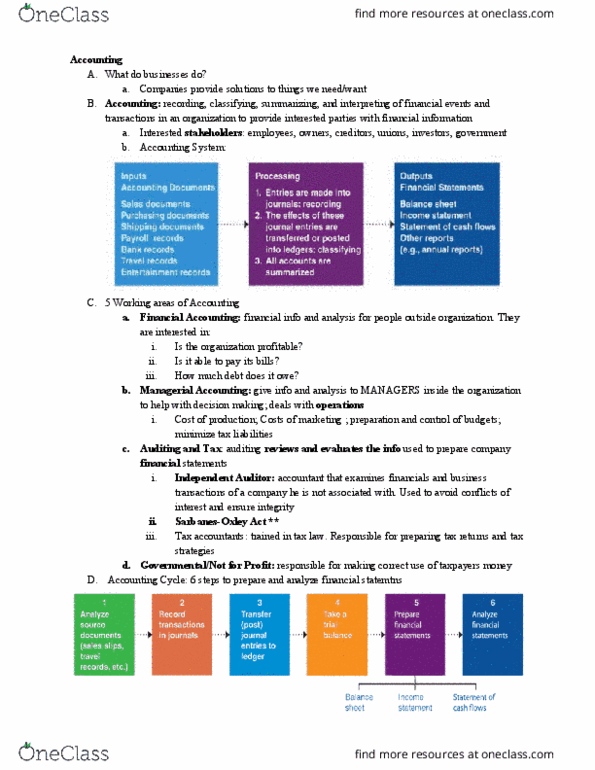

Accounting: recording, classifying, summarizing, and interpreting of financial events and transactions in an organization to provide interested parties needed financial information. Interested stakeholders employees, owners, creditors, unions, investors, and the government. (cid:373)ake use of a fir(cid:373)"s a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g i(cid:374)for(cid:373)atio(cid:374) Inputs: (accounting documents: sales documents, purchasing documents, shipping documents, payroll records, bank records, travel records, entertainment records. Processing: entries are made into journals, effects of these journal entries are transferred or posted into ledgers; classifying, all accounts are summarized. Outputs: (financial statement: balance sheet, income statement, statement of cash flows, other reports. 5 different areas of accounting: financial accountings, financial information and analyses generated for people primarily outside the organization. Income statements: the financial statement that sho(cid:449)s a fir(cid:373)"s (cid:271)otto(cid:373) li(cid:374)e that is its profit after costs, expenses, and taxes, revenue expenses = net income (profit or loss, selling/administrative expenses, promotion/advertising expenses, sales revenue.