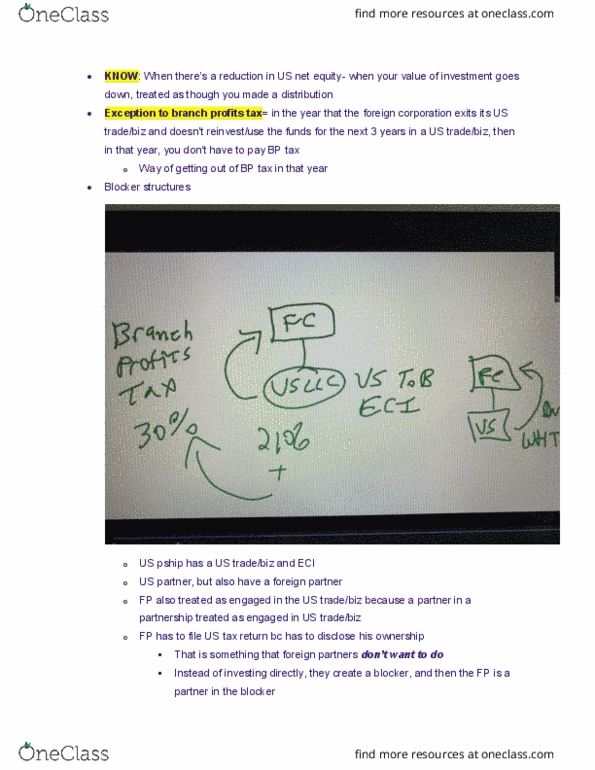

TAX 9869 Lecture Notes - Lecture 56: Double Taxation, Model Treaty, Iced Tea

Document Summary

Of benefit clause (reviewed many articles in the treaty) Generally speaking (context of fp doing biz in the us) but to be clear treaties cover both sides (us person doing biz in another country) Whenever fp doing biz in us or us doing biz in fc, concern that a taxable presence is created. Fp created a us taxable presence which is based on facts/circum. And they have a us tob they are subj to us tax on eci (statutory law// that"s what it says in irc + regs) If however, you are dealing w/ for ex. Fp is doing biz in us but fp is a resi of a country that has an. Itax treaty w/ us and that fp who is a resi of that country also meets limitation on benefits clauses (eligible for treaty benefits) Once you deal w/ treaty benefits you are out of the standards of us tob/eci and now talking about permanent establishment (pe)