TAX 9869 Lecture Notes - Lecture 31: Tax Treaty, Intangible Property, Tax Rate

Document Summary

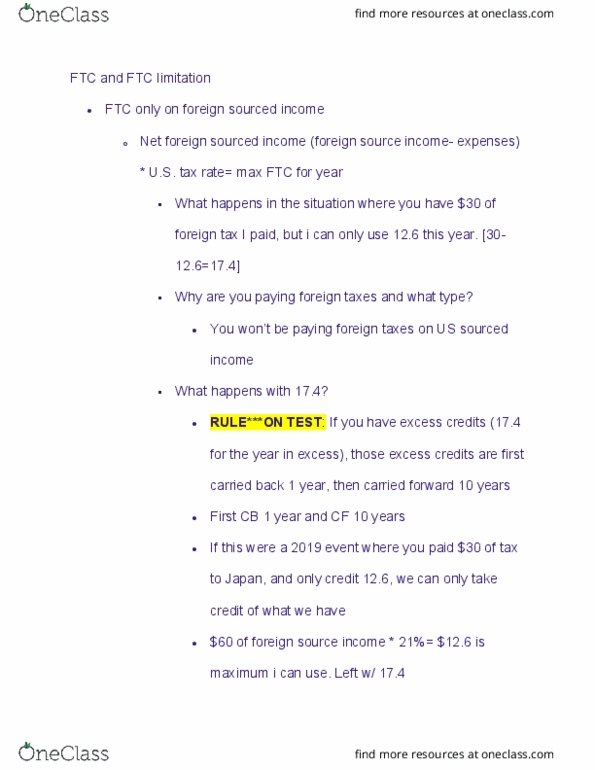

One has a choice to take credit or deduction. In the same year you cannot do both: cannot take a credit for some ft and deduction for other ft (foreign taxes, every year its a choice (credit or deduction, ex: talked about ftc limitation. Can only take ftc against us tax liab on foreign source income: must have fsi, lets say not enough fsi (you are limited)- you have excess credits carryback 1 yr/fwd 10. Formula: ftc limitation: fsi * effective us tax rate (this will. This is the formula used irl; actual formula in code is different. Irc formula: fsi (net)/worldwide income * us tax you have to pay. Ex: person"s fsi = 1000, worldwide income = 5000, us tax to pay = Irc formula: 1000/5000 * 2,000 = 20% * 2,000 = 400. That"s the amount of foreign tax you can take. 40% tax rate = effective tax rate bc (2000/5000=40%)