ADMS 4541 Lecture Notes - Lecture 3: Income Statement, Retained Earnings, Collection Agency

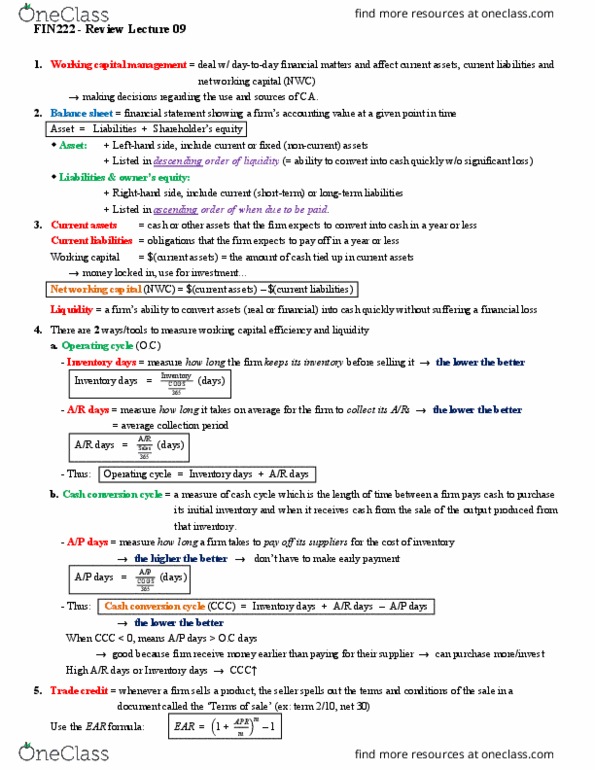

Document Summary

Get access

Related Documents

Related Questions

INSTRUCTION: Answer all questions in this section. Each question carries 2 marks. Answer True or False to the following questions.

1. The cash conversion cycle of a firm is the length of time between the actual cash outflow for materials and the actual cash inflow from sales. To calculate this cycle, we need all the information used to calculate the operating cycle plus Days Payables Outstanding (DPO).

2. Net working capital is defined as current liabilities minus current assets.

3. Sales volume and collection period will be affected by a firm's credit policy.

4. Accounts payable, or trade credit, increases net working capital.

5. Efficient cash management is often concerned with speeding up the collection of cheques received and slowing down the payment of cheques issued.

Choose the letter a, b, c, or d that carries the best response.

6. The income statement reports the results of operations during the past year, the most important item being:

Net Income

Interest Expense

Earnings Before Interest and Taxes

Earnings Per Share

7. Which would represent claims against assets in the balance sheet:

Liabilities

Liabilities and stockholders' equity

Common stockholders' equity

Both common and preferred stockholders' equity

8. The two accounts that normally make up the common equity section of the balance sheet are and

accounts payable; accruals

common stock; retained earnings

long-term bonds; common stock

equity; liabilities

9. Accounting profits is different from net cash flow because

Net cash flow includes profits from operations.

Non-cash items are not included in the accounting profits

Net-cash flows take account of all non-cash items

Accounting profits overlooks depreciation and taxes

| MGMT2023 | Page 3 |

10. Which of the following represents an investing cash outflow?

An increase in holdings of stocks of other companies

A decrease in accounts payable

A decrease in gross property, plant and equipment

A decrease in accumulated depreciation

11. Which group of ratios show the combined effect of liquidity, asset management and debt on operating results?

Liquidity ratios

Debt ratios

Coverage ratios

Profitability ratios

| 12. Cottler Ltd. has current. assets equal to $4.5 million. The company's current ratio is 1.25, and its quick ratio is 0.75. What is the firm's level of current liabilities in millions | |

| $3.6 | |

| $0.18 | |

| $2.4 | |

| $2.9 | |

13. You are given the following cash flows. What is the present value (t = 0) if the discount rate is 12 percent?

| Time | 0 | 1 | 2 | 3 | 4 | 5 | 6 |

| Cash flows | 0 | 1,000 | 2,000 | 2,000 | 2,000 | 0 | -2,000 |

| PV= ? | |

| $3,277 | |

| $4,169 | |

| $5,302 | |

| $4,289 |

14. You invest $5,000 today. You will earn 8% interest. How much will you have in 4 years? (Pick the closest answer.)

| $6,802 | |

| $6,843 | |

| $3,675 | |

| $3,475 |

15. You are buying your first house for $220,000 and are paying $30,000 as a down payment. You have arranged a 30-year mortgage loan With a 7% nominal interest rate and monthly payments. What are the equal monthly payments you must make?

| $1,513 | |

| $1,464 | |

| $1,264 | |

| $6,922 |

| Balance Sheet | 2015 | 2016 | 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | 807,000 | 628,000 | 612,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts Receivables | 2,582,000 | 2,896,000 | 4,605,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Inventories | 2,870,000 | 5,181,000 | 7,319,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Current Assets | 6,259,000 | 8,705,000 | 12,536,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Fixed Assets | 2,216,000 | 2,423,000 | 5,538,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Assets | 8,475,000 | 11,128,000 | 15,074,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Liabilities and Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts Payable | 961,000 | 1,648,000 | 3,137,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Notes Payable | 400,000 | 800,000 | 2,860,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accruals | 440,000 | 800,000 | 1,150,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Current Liabilities | 1,801,000 | 3,248,000 | 7,147,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Long Term Debt | 1,350,000 | 1,908,000 | 1,867,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | 3,650,000 | 3,650,000 | 3,650,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retained Earnings | 1,674,000 | 2,322,000 | 2,410,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Equity | 5,324,000 | 5,972,000 | 6,060,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Liabilities and Equity | 8,475,000 | 11,128,000 | 15,074,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Income Statement | 2015 | 2016 | 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | 26,820,000 | 28,966,000 | 30,703,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cost of Sales | 21,216,000 | 23,550,000 | 26,140,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gross Profit | 5,604,000 | 5,416,000 | 4,563,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Expenses | 2,574,000 | 3,225,000 | 3,866,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Profit | 3,030,000 | 2,191,000 | 697,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Interest | 91,000 | 275,000 | 469,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Earnings Before Taxes | 2,939,000 | 1,916,000 | 228,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Taxes (48%) | 1,411,000 | 919,000 | 110,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Income | 1,528,000 | 997,000 | 118,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ABC Company, a toy manufacturer, believes the coming holiday season (between Thanksgiving in late November and Christmas on the 25thof December) will be a very good one, expecting an increase of 20% in its sales. Outside economic analysts believe the effects of the recent recession are over. Consumer confidence is high. To meet that 20% increase, however, inventories must be built up so, to finance that expansion, ABC wants to borrow $1,000,000 from its bank.

You are the loan officer who must make the decision as to whether or not to give ABC the money. You are going to prepare ratios for 3 years, the Cash Conversion Cycle for the same period and operating cash flow for the years for which you have figures.

Review the Balance Sheets and Income Statements for ABC over the 3 years and answer the following questions (20 points each).

3) Operating Cash Flow is the first of the 3 parts to the Statement of Cash Flows.

a) Define operating cash flow. What does it tell us?

b) Calculate ABCâs operating cash flows for those years for which figures are available.

c) Does your analysis of ABCâs operating cash flows change your conclusions listed in 1) and 2) above?

4) Do you believe ABCâs cash position and its management of cash needs improvement? If so, how would you recommend they do it?

Answer Questions in Bold!