ADMS 3595 Lecture Notes - Lecture 6: Deferral, Current Liability, Unearned Income

ADMS 3595 Solutions to Self Practice Questions

1

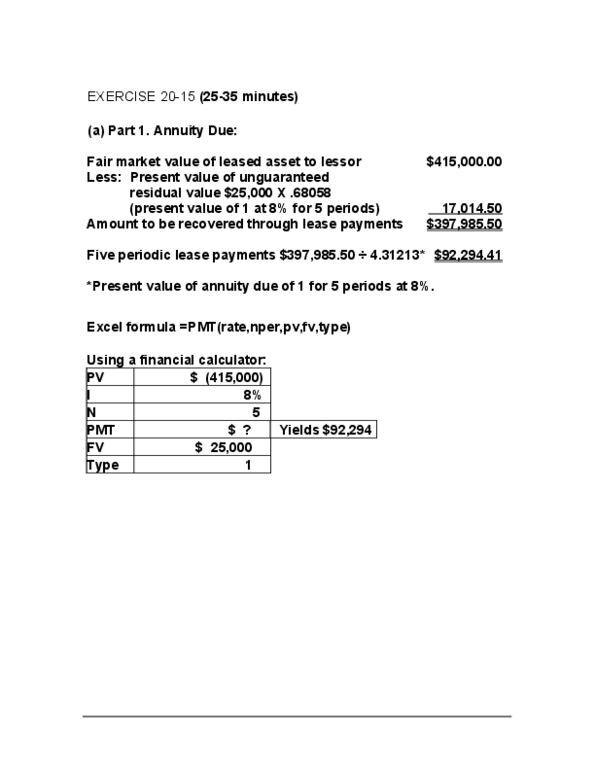

EXERCISE 20-1

(a) Initial Measurement of Right-of-Use Asset and Lease Liability

Contractual Rights and Obligations under Lease,

Jan. 1, 2017

Annual lease payment:

Yearly payment $73,580.00

Executory costs 2,470.29

Annual lease payment $71,109.71

Present value of lease payments

$71,109.71 X 6.32825 = $450,000.00

Excel formula =PV(rate,nper,pmt,fv,type)

Using a financial calculator:

PV

$ ?

Yields $450,000

I

12%

N

10

PMT

$ (71,109.71)

FV

$ 0

Type

1

1/1/17 Right-of-Use Asset ............................................ 450,000.00

Lease Liability .................................... 450,000.00

(b)

MALEKI CORP.

Lease Amortization Schedule

(Lessee)

find more resources at oneclass.com

find more resources at oneclass.com

ADMS 3595 Solutions to Self Practice Questions

2

Date

Annual

Pmt. Excl.

Exec. Costs

Interest (12%)

on Unpaid

Liability

Reduction

of Lease

Liability

Balance

of Lease

Liability

$450,000.00

Jan. 1,

2017

$71,109.71

$71,109.71

378,890.29

Jan. 1,

2018

71,109.71

$45,466.83

25,642.88

353,247.41

Jan. 1,

2019

71,109.71

42,389.69

28,720.02

324,527.39

Jan. 1,

2020

71,109.71

38,943.29

32,166.42

292,360.97

Jan. 1,

2021

71,109.71

35,083.32

36,026.39

256,334.58

Jan. 1,

2022

71,109.71

30,760.15

40,349.56

215,985.02

Jan. 1,

2023

71,109.71

25,918.20

45,191.51

170,793.51

Jan. 1,

2024

71,109.71

20,495.22

50,614.49

120,179.02

Jan. 1,

2025

71,109.71

14,421.48

56,688.23

63,490.79

Jan. 1,

2026

71,109.71

7,618.92

63,490.79

0

$711,097.10

$261,097.10

$450,000.00

(c)

1/1/17 Insurance Expense ........................................... 2,470.29

Lease Liability ................................................... 71,109.71

Cash .................................................. 73,580.00

12/31/17 Depreciation Expense ....................................... 45,000.00

Accumulated Depreciation—

Right-of-Use Asset ........................ 45,000.00

($450,000 ÷ 10)

12/31/17 Interest Expense ......................................... 45,466.83

Lease Liability .................................... 45,466.83

1/1/18 Insurance Expense ......................................... 2,470.29

Lease Liability ................................................. 71,109.71

Cash .................................................. 73,580.00

12/31/18 Depreciation Expense .................................... 45,000.00

Accumulated Depreciation—

Right-of-Use Asset ........................ 45,000.00

12/31/18 Interest Expense............................................. 42,389.69

Lease Liability ................................... 42,389.69

(d) Note X: The following is a schedule of future lease payments under a contract-based

lease liability expiring December 31, 2026 together with the balance of the lease liability.

find more resources at oneclass.com

find more resources at oneclass.com

ADMS 3595 Solutions to Self Practice Questions

3

Year ending December 31

2019 $73,580

2020 73,580

2021 73,580

2022 73,580

2023 73,580

2024 and beyond 220,740

Total lease payments 588,640

Less amount representing executory costs 19,763

568,877

Less amount representing interest at 12% 215,630

Balance of the lease liability $353,247

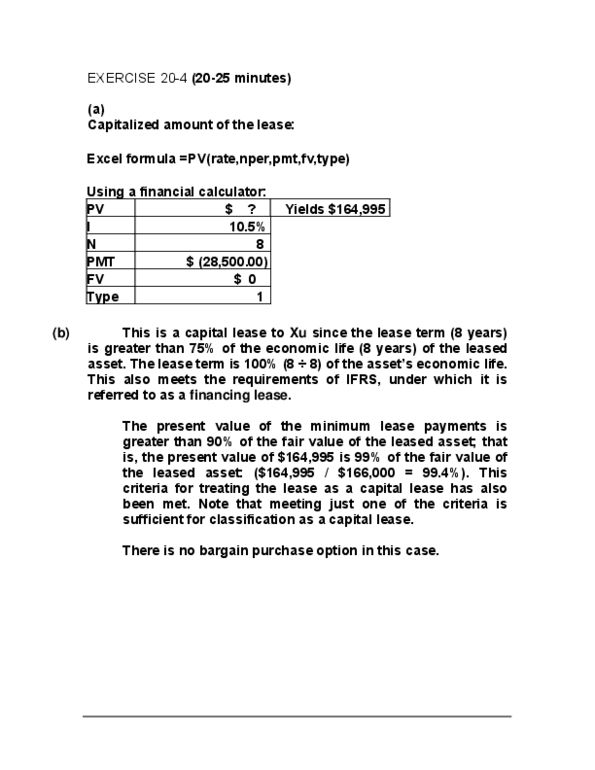

EXERCISE 20-3

(a) Initial Measurement of Right-of-Use Asset and Lease Liability

Contractual Rights and Obligations under Lease,

July 1, 2017

$20,066.26Annual rental payment

X 4.23972 PV of annuity due of 1 for n = 5, i = 9%

$85,075.32PV of periodic rental payments

$ 4,500.00Bargain purchase option

X .64993 PV of 1 for n= 5, i = 9%

$ 2,924.69PV of bargain purchase option

$85,075.32PV of periodic rental payments

+ 2,924.69 PV of bargain purchase option

$88,000.01Net investment at inception of lease

Excel formula =PV(rate,nper,pmt,fv,type)

Using a financial calculator:

PV

$ ?

Yields $ 88,000

I

9%

N

5

PMT

$ (20,066.26)

FV

$ (4,500)

Type

1

(b) The lease would be set up as a right-of-use asset and lease liability under IFRS 16 as it

would not qualify for a short-term or low-value exemption.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

42,389. 69 (d) note x: the following is a schedule of future lease payments under a contract-based lease liability expiring december 31, 2026 together with the balance of the lease liability. Initial measurement of right-of-use asset and lease liability. Pv of annuity due of 1 for n = 5, i = 9% Pv of 1 for n= 5, i = 9% 1 (b) the lease would be set up as a right-of-use asset and lease liability under ifrs 16 as it would not qualify for a short-term or low-value exemption. The lease agreement has a purchase option that is reasonably certain to be exercised. The collectability of the lease payments is reasonably predictable, and there are no important uncertainties surrounding the costs yet to be incurred by the lessor. The present value of the minimum lease payments exceeds 90% of the fair value of the equipment.