ADMS 3300 Lecture Notes - Lecture 7: Conditional Probability, Perfect Information, Expected Value Of Perfect Information

17 Aug 2016

School

Department

Course

Professor

Document Summary

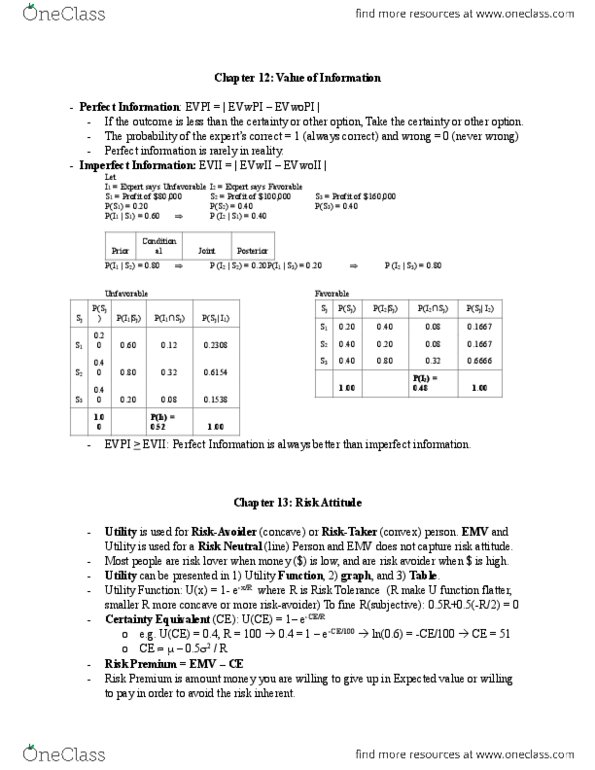

To answer these questions, we will have to determine the value of perfect information and imperfect information. Let a = do(cid:449) jo(cid:374)es i(cid:374)de(cid:454) and let (cid:862)a(cid:863) = expert says do(cid:449) jo(cid:374)es i(cid:374)de(cid:454) . P(cid:894) e(cid:454)pert sa(cid:455)s do(cid:449) jo(cid:374)es | do(cid:449) jo(cid:374)es (cid:895) = (cid:1005) P( (cid:862)a(cid:863)|a) = 1 1 p( (cid:862)a(cid:863)|a) p((cid:862)a(cid:863)|a) = 0. He(cid:374)(cid:272)e, p(cid:894)a|(cid:863)a(cid:863)(cid:895) = (cid:1005) (cid:374)o (cid:373)atter (cid:449)hat the (cid:448)alue of p(cid:894)a(cid:895) is, for all possi(cid:271)le out(cid:272)o(cid:373)es {a1, , an} If we knew si ={up, flat, do(cid:449)(cid:374)} (cid:449)ould happe(cid:374) For each scenario, determine the most optimal value (pick the best outcome) Evpi establish the upper bound/limit on the expected value of any information. Evpi = |ev with pi ev without pi| Maximum you are willing to pay for the perfect information is . Pr( {expert says dow jones } | {dow jones } ) = pr(a| a) < 1. True market state (conditional probability) (cid:862)up(cid:863) (cid:862)flat(cid:863) (cid:862)down(cid:863) Suppose the imperfect expert said dow jones will go up.