BU527 Lecture Notes - Lecture 6: Operating Cash Flow, Income Statement, Cash Flow Statement

Document Summary

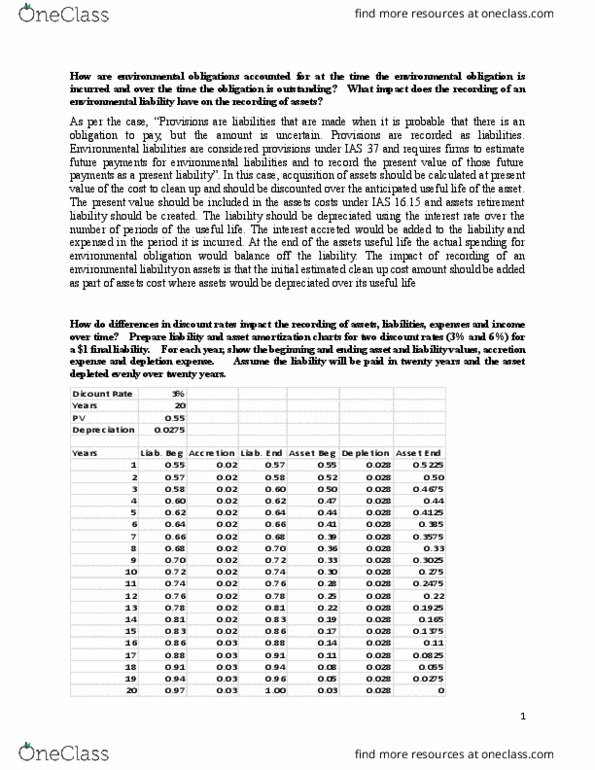

As per the case, provisions are liabilities that are made when it is probable that there is an obligation to pay, but the amount is uncertain. Environmental liabilities are considered provisions under ias 37 and requires firms to estimate future payments for environmental liabilities and to record the present value of those future payments as a present liability . In this case, acquisition of assets should be calculated at present value of the cost to clean up and should be discounted over the anticipated useful life of the asset. The present value should be included in the assets costs under ias 16. 15 and assets retirement liability should be created. The liability should be depreciated using the interest rate over the number of periods of the useful life. The interest accreted would be added to the liability and expensed in the period it is incurred.