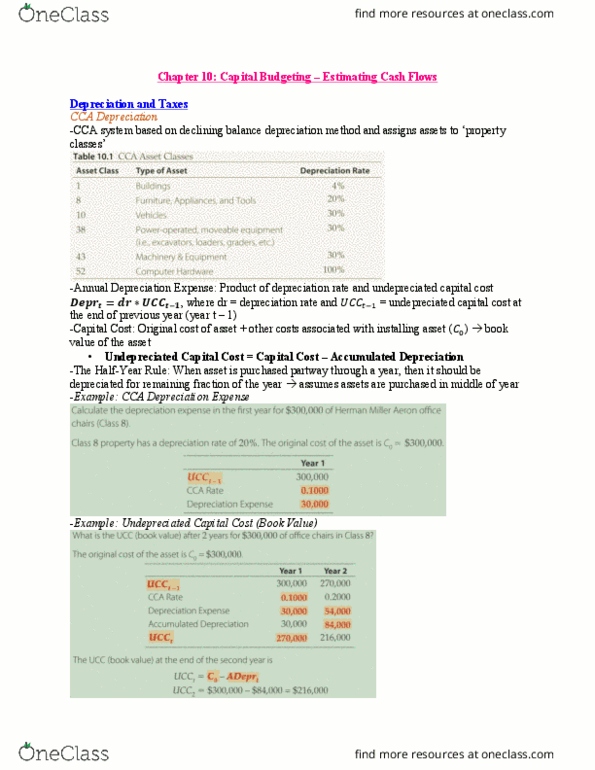

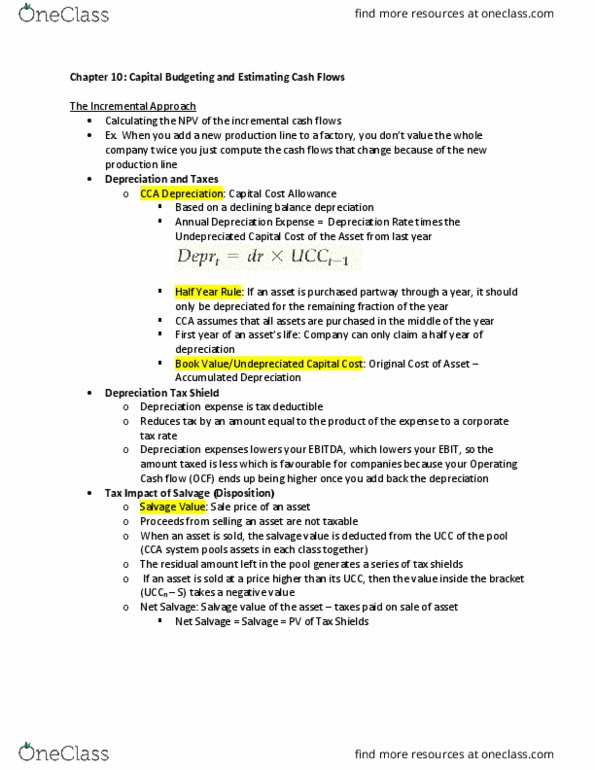

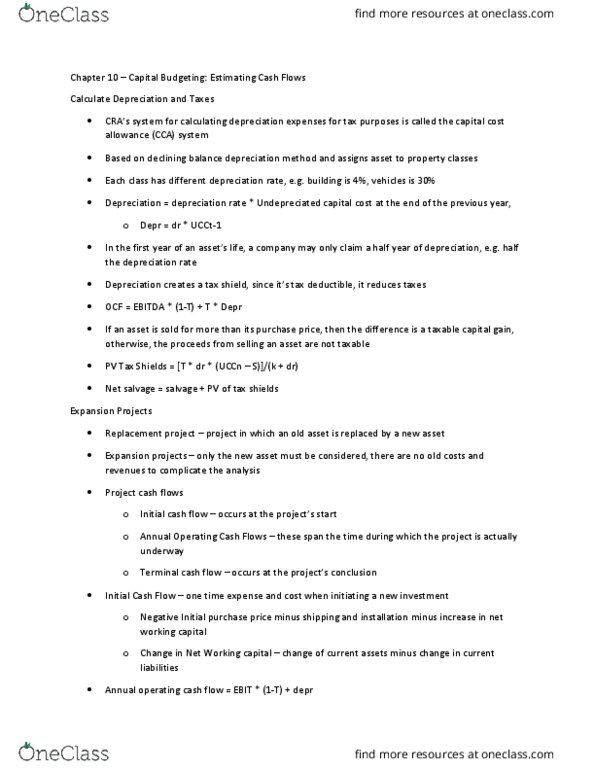

BU393 Lecture Notes - Lecture 5: Cash Flow, Net Present Value

10.3

Replacement Projects:

- To evaluate a replacement, we compare two scenarios:

1. Keeping old equipment

2. Replacing it

- Calculate cash flows with replacement and subtract cash flows that would have been

received with the old. The differences are the incremental cash flows from replacement

- To assess a replacement decision, we estimate the net present value of the incremental

cash flows – if NPV is positive, we replace

- At time 0, incremental cash flows are proceeds from selling old assets minus cost of

buying new

- In terminal year, we must get salvage value of new asset less the foregone salvage value

of the old asset

- When an asset is replaced, the CCA system adds the cost of the new machine to the

asset class and deducts the salvage value of the old machine – always increases the UCC

balance in that class. THERE ARE NO TAX IMPLICATIONS WITH PURCHASE OF THE NEW

ASSET OR THE SALE OF THE OLD ASSET

Operating Cash Flows:

- Incremental annual operating cash flows for a replacement are the difference between

the operating cash flows after replacement and the operating cash flows with old asset

- Difference between new depreciation expense and the old one is incremental

depreciation – amount that depreciation changes because of the purchase of the new

machine

- Change to the UCC of the class is the incremental capital cost, which is the cost of the

new machine minus the salvage value of the old machine. So the incremental

depreciation expense is the declining balance depreciation expense from the

incremental capital cost

Terminal Cash Flows:

- When the project ends the cash invested in the working capital is no longer needed and

is returned – so a decrease in net working capital is a positive cash flow in the terminal

year

Net Incremental Salvage:

- Difference between the salvage value of the new machine and the salvage value of the

old machine had it been kept in service = incremental salvage + PV of the tax shields –

tax shields foregone because the company did not sell old asset

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

To evaluate a replacement, we compare two scenarios: keeping old equipment, replacing it. Calculate cash flows with replacement and subtract cash flows that would have been received with the old. The differences are the incremental cash flows from replacement. To assess a replacement decision, we estimate the net present value of the incremental cash flows if npv is positive, we replace. At time 0, incremental cash flows are proceeds from selling old assets minus cost of buying new. In terminal year, we must get salvage value of new asset less the foregone salvage value of the old asset. When an asset is replaced, the cca system adds the cost of the new machine to the asset class and deducts the salvage value of the old machine always increases the ucc balance in that class. There are no tax implications with purchase of the new. Asset or the sale of the old asset.