BU387 Lecture Notes - Lecture 2: Financial Statement, Income Statement

Document Summary

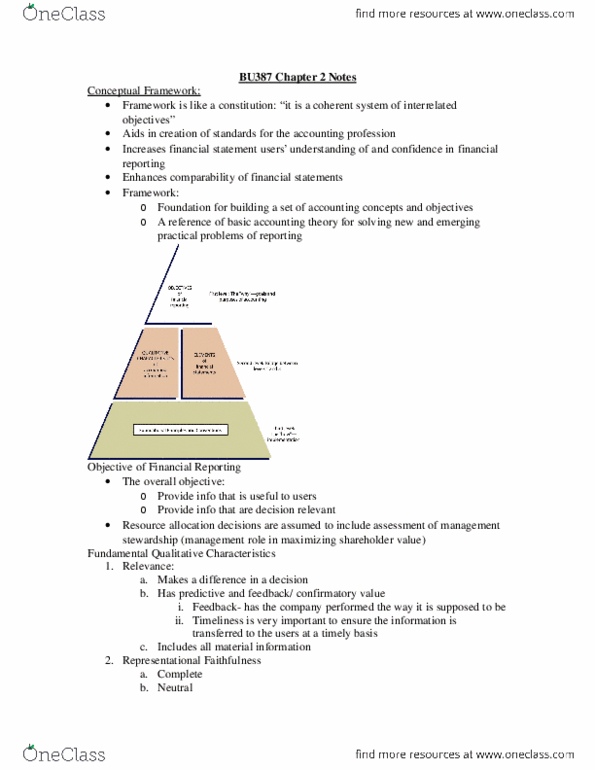

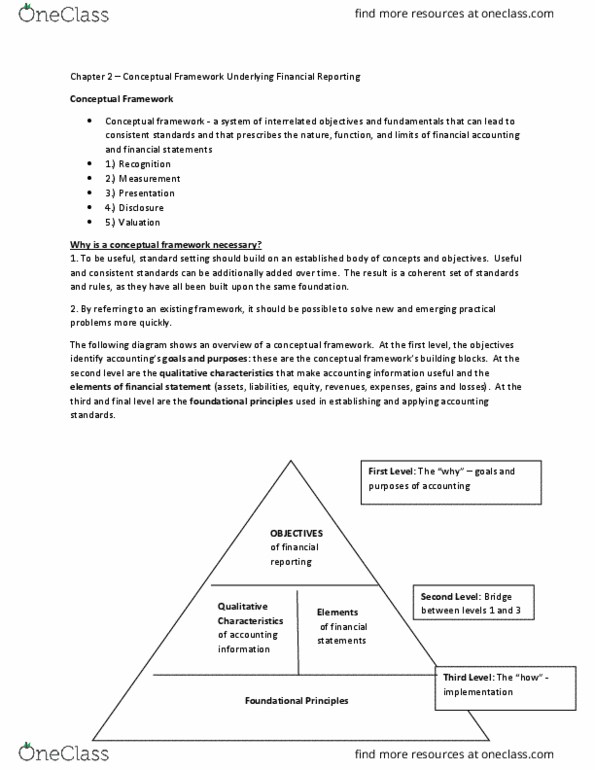

The fra(cid:373)e(cid:449)ork is like a (cid:272)o(cid:374)stitutio(cid:374); it is a (cid:862)(cid:272)ohere(cid:374)t s(cid:455)ste(cid:373) of i(cid:374)terrelated o(cid:271)je(cid:272)ti(cid:448)es(cid:863) I(cid:374)(cid:272)reases fi(cid:374)a(cid:374)(cid:272)ial state(cid:373)e(cid:374)t users" u(cid:374)dersta(cid:374)di(cid:374)g of a(cid:374)d confidence in financial reporting. Is the foundation for building a set of accounting concepts and objectives. Relevance: makes a difference in a decision, has predictive and feedback/confirmatory value. Representational faithfulness: complete and neutral, free from material error. Timeliness: public vs. private companies, public companies must issue financial reports within the financial period. Understandability: allows reasonably informed users to see the significance of the information. It is not always possible to have all fundamental and enhancing qualitative characteristics: trade-offs happen when one qualitative characteristics sacrificed for another. The benefits of using the information should outweigh the costs of providing that information. Involve some economic benefit to the entity: entity has a control over that benefit, benefit results from a past transaction or event.