BU283 Lecture Notes - Lecture 12: Budget Constraint, Astrium, Harry Markowitz

Document Summary

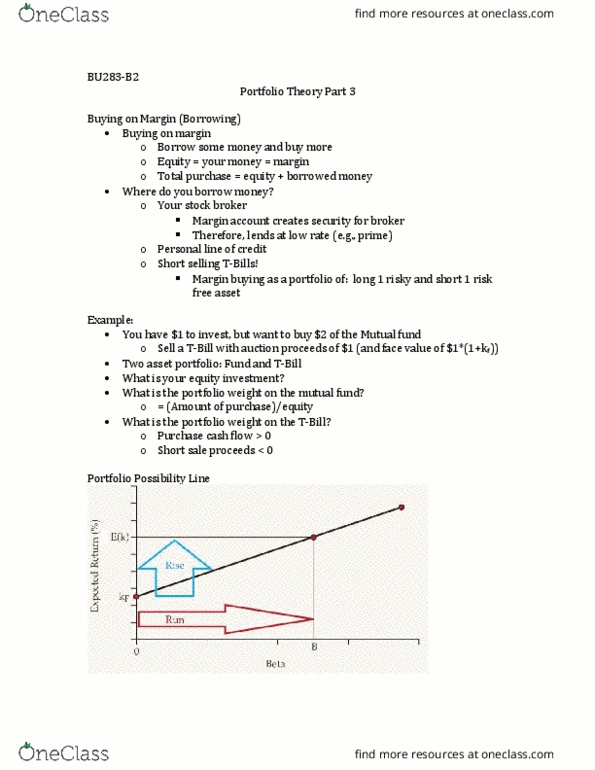

Consider a 2 asset portfolio: k p (1 kx. You have a two-asset portfolio with stocks a and b. You have 25% of your wealth in stock a and the correlation between the stocks is 1. P = [(0. 25^2)x(0. 04^2) + (0. 75^2)x(0. 10^2) + 2x0. 25x0. 75x(- These are the feasible combinations of return and risk available with the two assets, a and b, when their correlation is 1. These are the feasible combinations of return and risk available with the two assets, a and b, when their correlation is 0. Curve should be shaped like the letter "c" Plot the five pairs of points from your table above on the following graph. These are the feasible combinations of return and risk available with the two assets, a and b, when their correlation is +1. ______________, you cannot form a portfolio that has less standard deviation than the asset with the lowest standard deviation: +1, 1, 0.