BU127 Lecture Notes - Lecture 9: Internal Control, Cash Flow, Uptodate

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

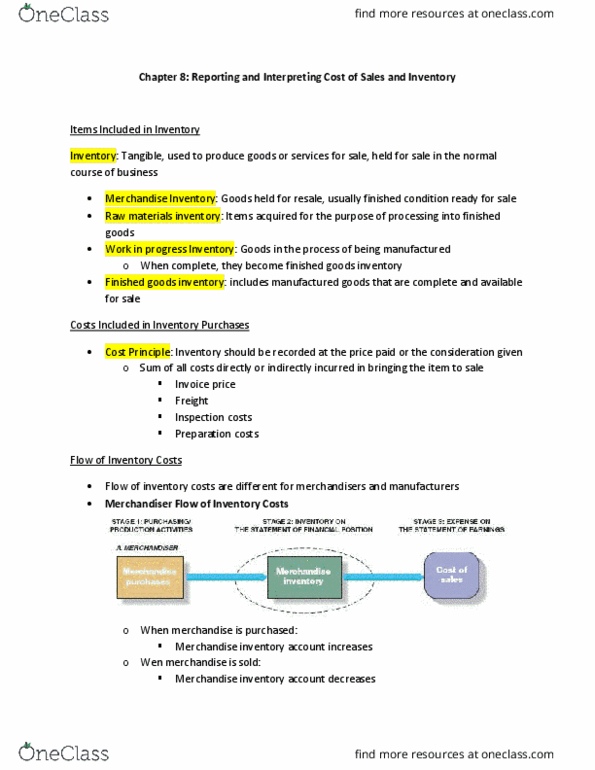

Chapter 8 reporting and interpreting cost of sales and inventory. Cost principle requires that inventory be recorded at price paid, includes all costs incurred to bring the asset to useable/saleable condition: invoice price, freight\inspection costs, preparation costs. Direct labour: earnings of employees who work directly on the products being manufactured factory overhead: manufacturing costs that are not raw material or direct labour costs. Cos = beginning inventory + purchases ending inventory. Provides up-to-date inventory records and cost of sales records. Purchase transactions are recorded directly into an inventory account. When each sale is recorded, cost of sale entry is made decreasing inventory: in periodic system, ending inventory and cost of sales are determined at end of accounting period based on physical count. Beginning inventory + purchases = cost of goods available for sale cos = ending inventory. Determined by the end of accounting period. Companies do not maintain an ongoing record of inventory during the year.