BU127 Lecture Notes - Lecture 11: Retained Earnings, Cash Flow, Accounts Receivable

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

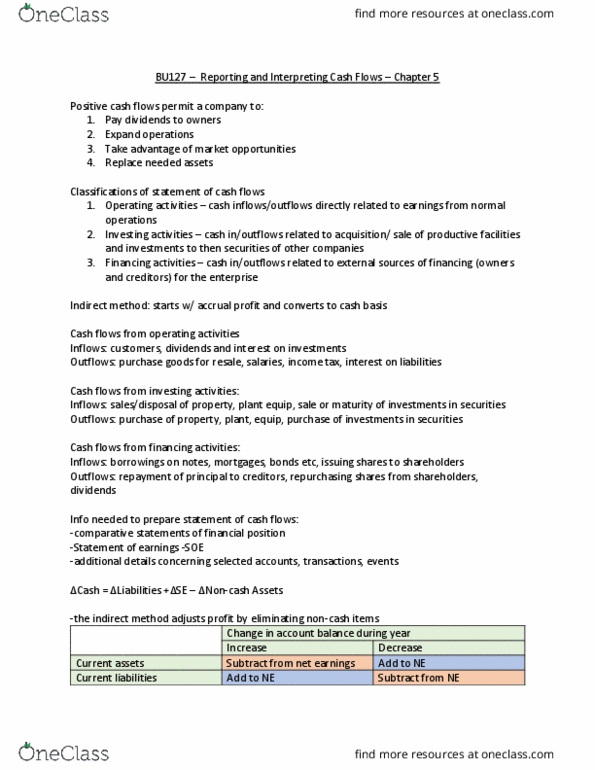

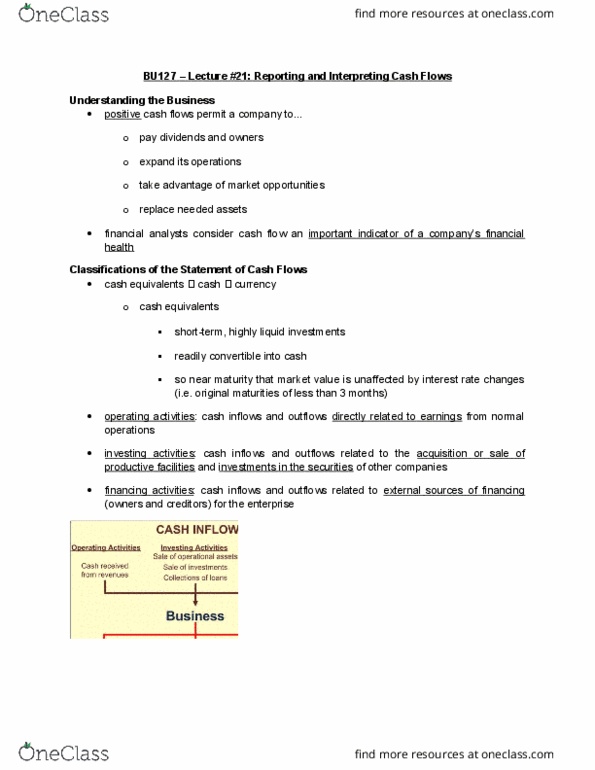

Classifications of the statement of cash flows: cash, cash equivalents, short-term, highly liquid investments, currency, 3 activities, operating activities, cash inflows and outflows directly related to earnings from normal operations. Indirect method: used by 99. 5% of companies, the ending balance should agree with the statement of financial position, adjust profit to compute cash flows from operating activities, starts with accrual profit and converts to cash basis. Direct method: not commonly used, reports components of cash flows from operating activities as gross receipts and gross payments, reports cash effects of each operating activity, generally more expensive to implement than the indirect method. Inflows: cash received from, customers, dividends and interest on investments, outflows, cash paid for, purchases of goods for resale and services, salaries and wages. Inflows: cash received from, sale or disposal of ppe, sale or maturity of investments in securities, outflows, cash paid for, purchase of ppe, purchase of investments in securities.