BU111 Lecture Notes - Lecture 7: Savings Account

19

BU111 Full Course Notes

Verified Note

19 documents

Document Summary

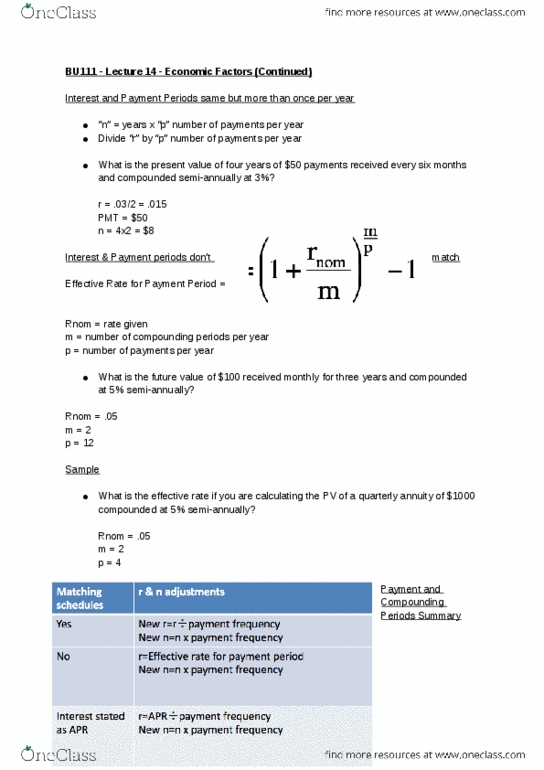

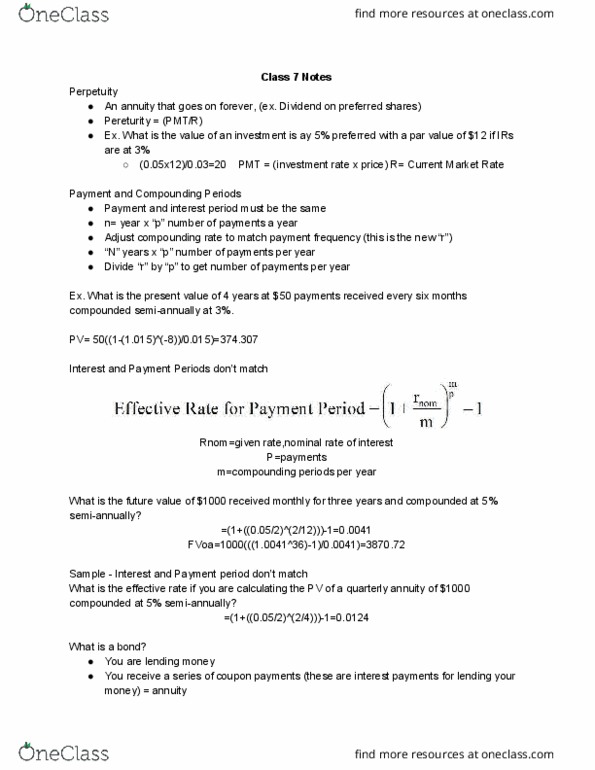

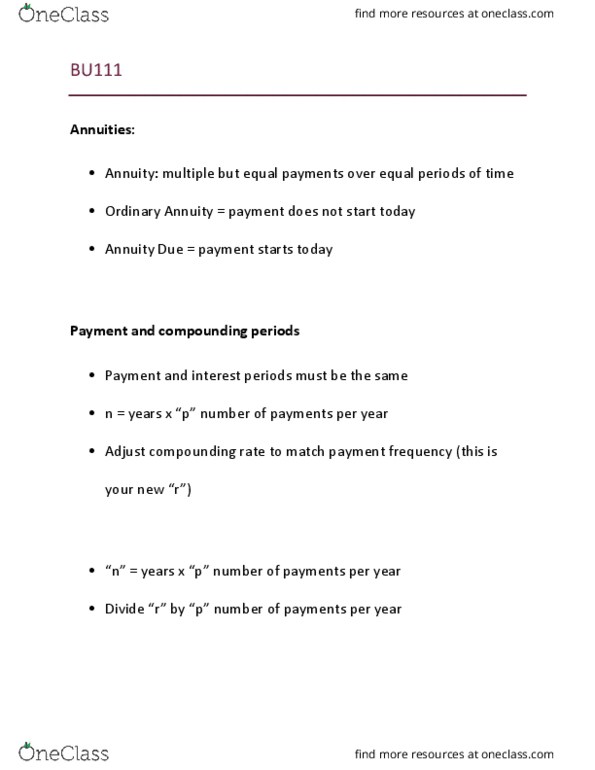

Payment and compounding periods: payment and interest periods must be the same, n= years x p number of payments per year, adjust compounding rate to match payment frequency (new r ) Assume interest/discount rate of 4% compounded semi- annually: pvoa= pmt (1/r-1/r(1+r)^n, pvoa= 500(1/. 02-1/. 02(1+0. 2)^6)=2800. 72. Assume interest/discount rate of 4% compounded quarterly: 4=. 04, pmt= 500, n=3 (x 12= 36, calculate effective rate for payment periods (1+rnom/m)^m/p-1, and then effective monthly rate (1+. 04/4)^12-1= 0. 0033, pvoa(500(1/. 0033-1/. 0033(1+. 0033)^36, = 16,938. 77. Interest and payments happen at the same frequency annually if not explicitly states r=. 105/2=. 0525: n=10x2= 20, plug numbers into formulas, solving for a bond we look for pvsa + pvoa. Mortgages how much principal do you still owe when the mortgage is renewed at the end of 5 years: pvoa= pmt (1/r-1/r(1+r)^n, =1599. 52(1. 0049 . 1/. 0049 (1. 0049 )^240: = 224,592. 24: how much we still have owing.