Management and Organizational Studies 3199Y Lecture 6: Solutions+-+Chapter+6

7 Jun 2017

School

Department

Professor

Document Summary

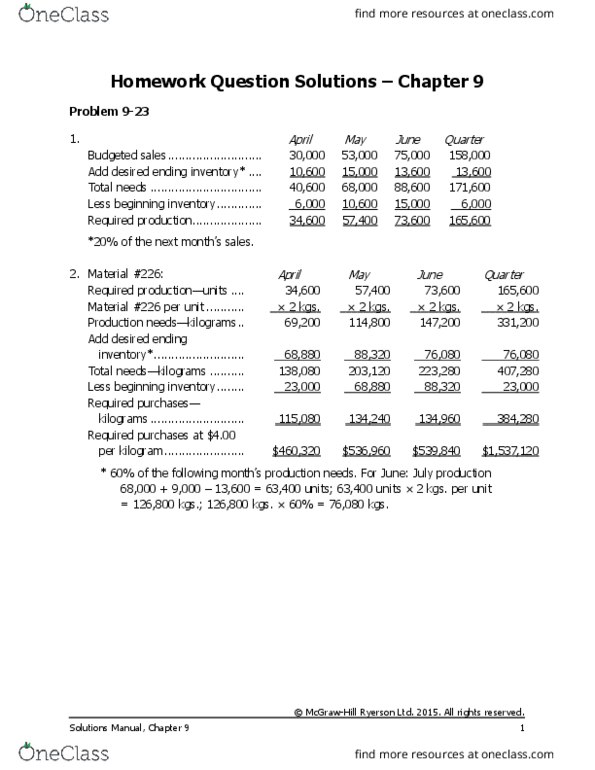

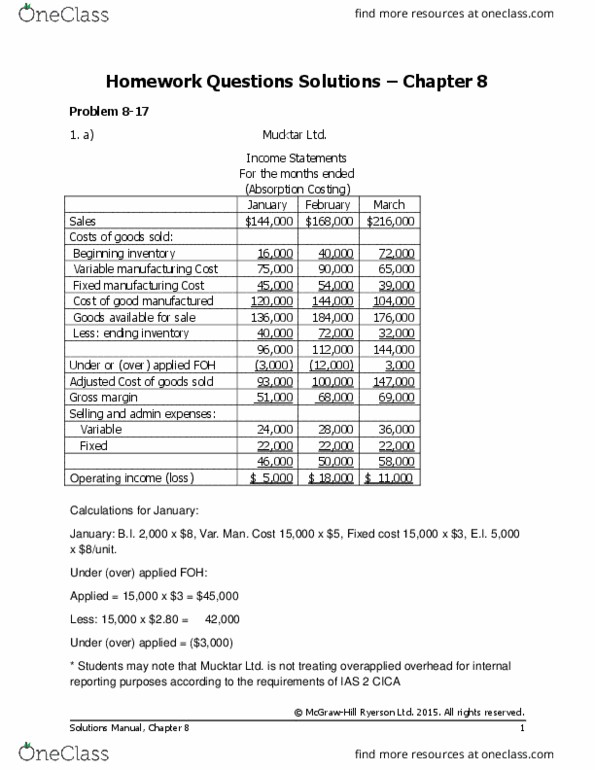

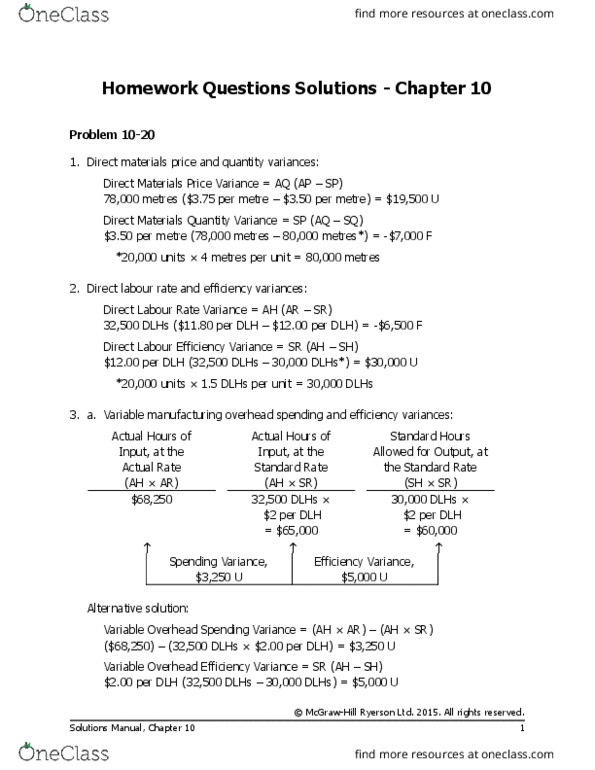

Cost per equivalent unit, (a) (b) Equivalent units of production (materials: 100,000 units 60% complete; conversion: 100,000 units 40% complete) Cost of ending work in process inventory Cost of units completed and transferred out Cost of beginning work in process inventory (,500 + ,000) Costs added to production during the period (,500 + ,000) Ending work in process: cost per equivalent unit, see the next page, cost reconciliation. Cost per equivalent unit (a) (b) To complete beginning work in process: equivalent units of production. Materials: 50,000 units (100% 75%) Conversion: 50,000 units (100% 30%) Units started and completed during the period (430,000 units started 100,000 units in ending inventory) Costs of ending work in process inventory and units transferred out. Cost in beginning work in process inventory Cost to complete the units in beginning work in process inventory: Equivalent units of production required to complete the. Cost of units started and completed this period: beginning inventory 12,500.