Management and Organizational Studies 3370A/B Lecture 3: Lecture 3

7 Oct 2016

School

Department

Professor

Document Summary

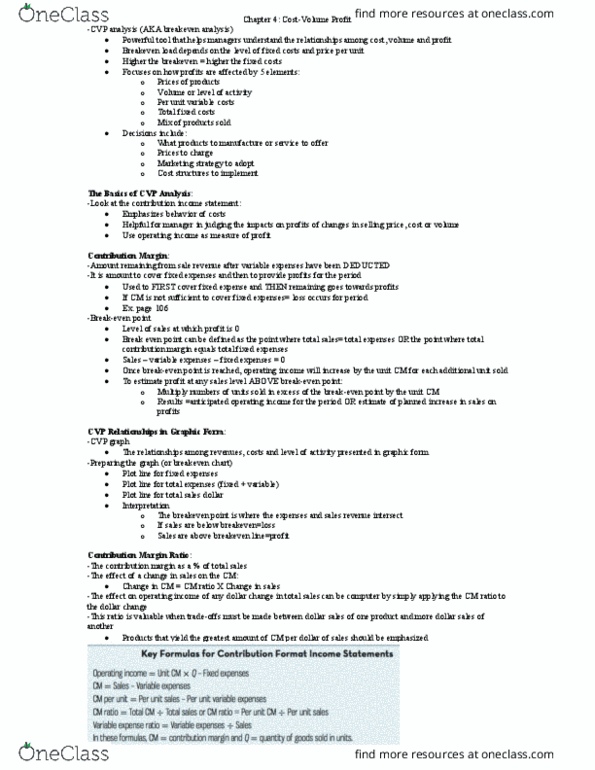

Lecture 3 chapter 3 continued, chapter 4. Traditional income statement is organized by function and fixed/variable costs are not distinguished. Separating costs into fixed and variable elements is often crucial in making decisions. Contribution margin is meant to cover fixed costs and any profit. Contribution income statement format is used as an internal planning and decision making tool: cost-volume-profit analysis (ch4, budgeting (chapter 9), segmented reporting of profit data (chapter 11), special decisions such as pricing and make-or-buy analysis (chapter 12). Contribution income statement is helpful to managers in judging the impact on profits of changes in selling price, cost, or volume. Contribution margin (cm) is the amount remaining from sales revenue after variable expenses have been deducted. Sales, variable expenses, and contribution margin can also be expressed on a per unit basis. additional cm will be generated to cover fixed expenses and profit.