Management and Organizational Studies 2277A/B Lecture Notes - Lecture 7: Down Payment, Opportunity Cost

27 Dec 2015

School

Department

Professor

Document Summary

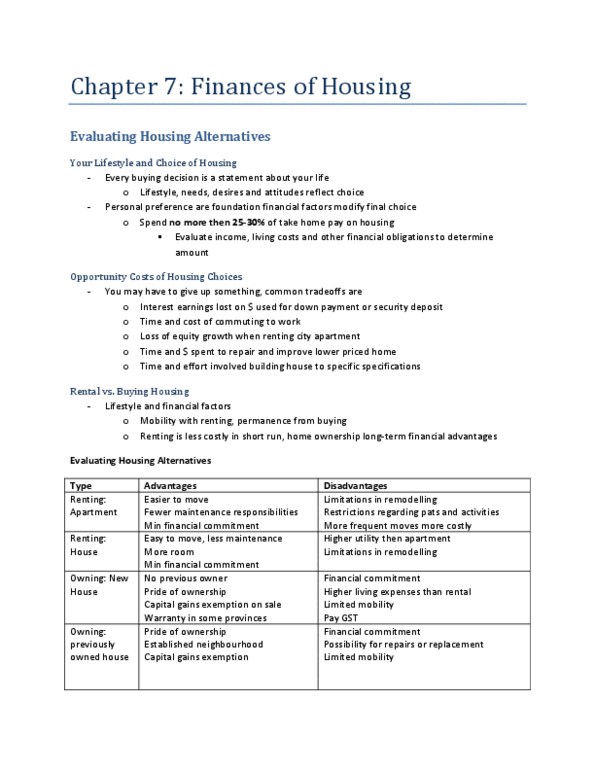

Wednesday, november 11, 2015. Buying/rent a home are financial alternatives. Saving vs paying down debt. Simple monthly payments (sometimes all- inclusive because of demand, but it"s throwing money away) Inexpensive upfront (big deal for calculations) More flexible (most important: not tied down to one place, small details vary) Less risk with short term value volatility. Fear of canadian housing bubble, overvalued. Building equity in an appreciating asset (automatic savings/retirement plan, but renting can build equity in other ways) Borrowing cheaply (each mortgage payment increases net worth, automatically) House flipping: treat as business income, not capital gains. Only applies to your own principle residence (only allowed to have one at a time) Sell, but you have to still live somewhere. Regular mortgage payments over the 4 years, but not completely paid off. , 500 appreciation - 5000 selling cost = 18500 return. ,500/,075 (out of pocket) = 153% Can massively amplify gains/losses by using leverage.