Business Administration 2257 Lecture Notes - Lecture 2: Contribution Margin, Income Statement, Variable Cost

28 Jan 2016

School

Department

Professor

Document Summary

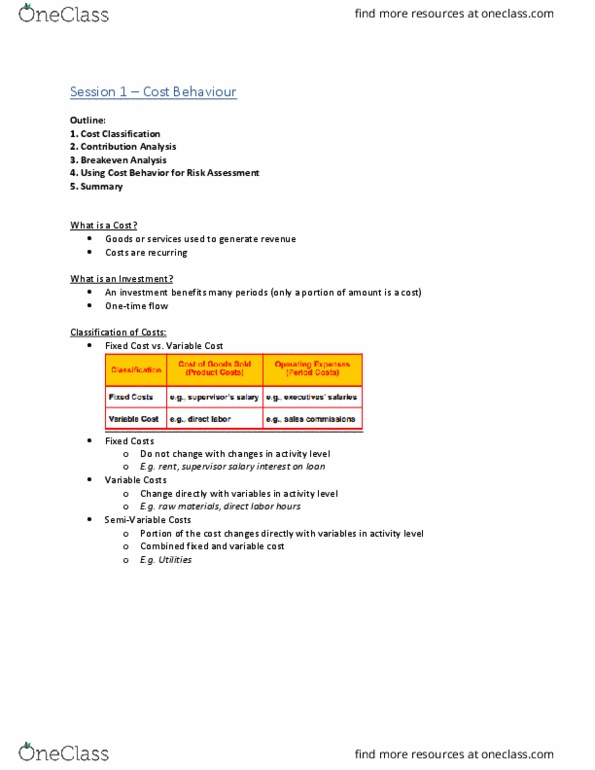

Uses of contribution analysis: breakeven analysis. Weighted-average: using cost behaviour for risk assessment: Classification exercise: goods or services used to generate revenue, a recurring flow. Investment: benefits many periods (only a portion of amount is a cost, a one-time flow. Do not change with changes in activity level. Change directly with changes in activity level. A portion of cost that change directly with variables in activity. Income statements can be presented in more than one way depending on how costs are classified. The term 1 statement classifies costs as product or period; whereas, the income statement, on a contribution basis, classifies costs as fixed or variable. Definition: the amount that the sale of one unit of product contributes toward recovery of the fixed costs and then toward a profit. I. e. , the amount by which the sales price per unit exceeds the costs incurred specifically to produce and sell that unit. Unit contribution = selling price variable cost per unit.