RSM432H1 Lecture Notes - Lecture 9: Yield Spread, Market Risk, Survival Analysis

Document Summary

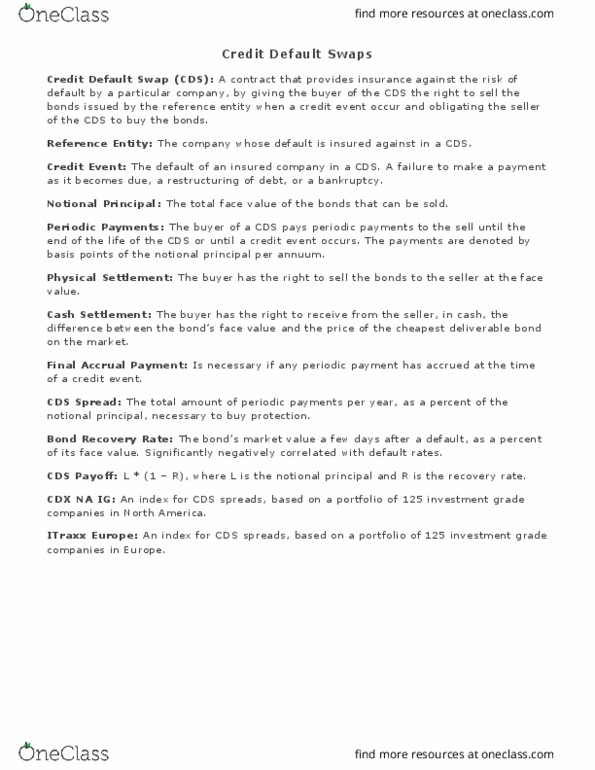

Bond yields are indication of market"s perceived risk. Looks at equity as an option on company. Distance to default tries to express probability of default on a forward looking basis. Contrasts to historical data, which is backward looking. Hazard rate/default intensity ( (t): probability of default over short time period conditional on no earlier default. Unconditional default probability: probability of default as seen at time zero. Price of bond 30 days after default as percent of face value. Probability of default between t and t+ t conditional on no earlier default: Buyer acquires protection from seller against default by a particular company or country. Seller pays out amount not paid out by entity in event of default. Cds market allow credit risk to be traded, similar to market risk. Cdss and cds indices trade increasingly like bonds, becoming more standardized.