RSM424H1 Lecture Notes - Lecture 8: Share Capital, Capital Loss

Document Summary

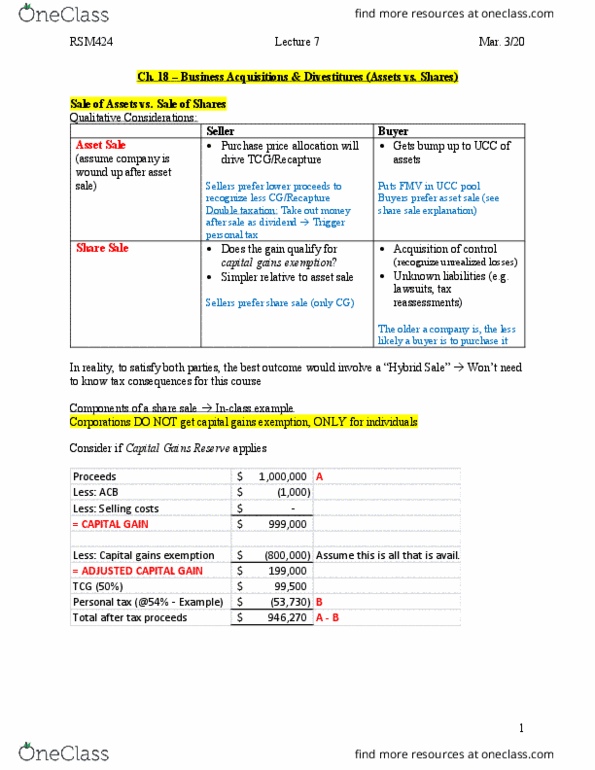

18 business acquisitions & divestitures (assets vs. shares) Recap: capital gains exemption: sbc test, holding period test, basic asset test. Alternative 1 shares of subpump are sold. Conclusion: shares qualify for capital gains exemption since shares are qsbc shares. Capital gain deduction of ,456 comes from remaining exemption" (see below) Clowes already claimed the maximum capital gains deduction last year. Capital gain deduction (cgd) claimed against tcg, as opposed to cg. Exists to prevent claim of abils, ncls and cgd on the same gain. Less: previous abil claims: cumulative gains limit. Cnil example: interest deduction borrow money to invest in qsbc shares, but don"t earn return or any other investment income, investment losses are allowed. Prevents double claim of investment losses and interest deductions. Step 1: determine type of income (fill out chart) Grip: pool tracking amount that ccpc can pay eligible dividends out of, any amount greater than grip is non-eligible.