RSM230H1 Lecture Notes - Lecture 9: Credit Risk, Downside Risk, Spot Contract

26 Nov 2016

School

Department

Course

Professor

Document Summary

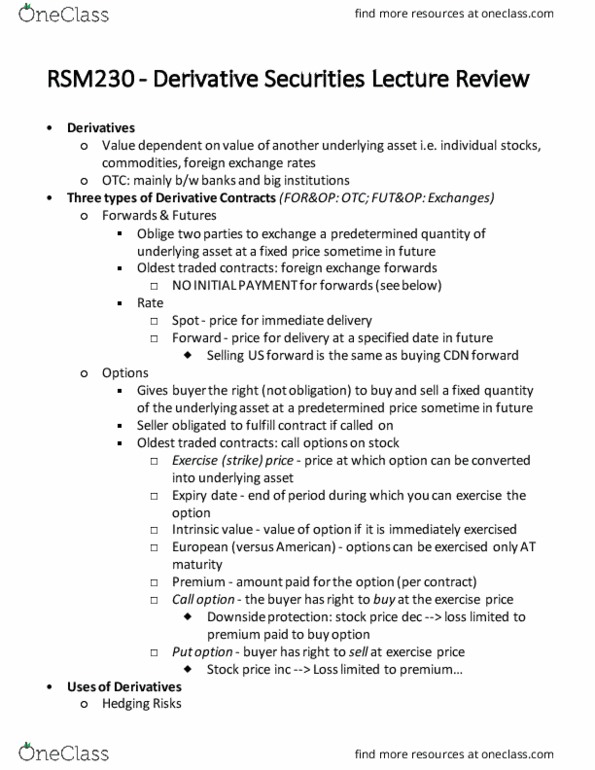

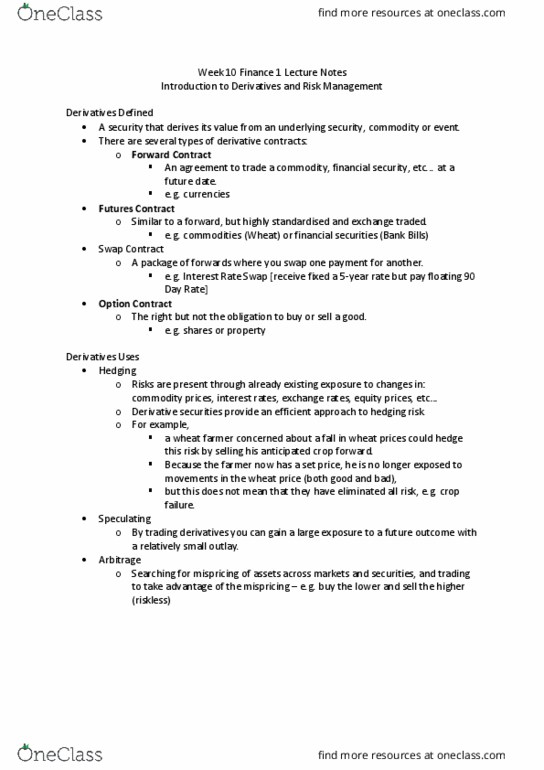

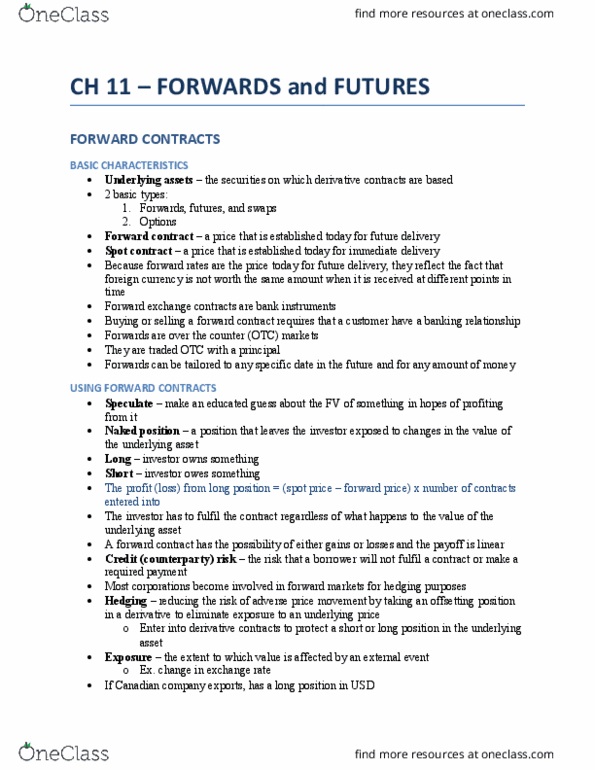

Derivative contract -> b is based on a (if a moves, b moves too) Esta(cid:271)lish ter(cid:373)s (cid:894)pri(cid:272)e, date, deli(cid:448)er(cid:455) (cid:895) today for a transaction in the future. Copper delivered in a month, set prices today -> it is a derivative contract. Borrow , interest = to pay back. An agreement between the producer and buyer to establish the price ahead of time. Derivative contract only reallocate risks but not removing risks. 98% of business get to use hedging, others are speculating. Short exposure = you owe something x-axis = price of underlying issue. In long position: if price goes up due to risk exposure only, you profit. If y=0, it does not mean i have no profit at all, it only means i have no profit due to risk exposure. In short position: price going down due to risk exposure is better.