ECO101H1 Lecture Notes - Lecture 16: Perfect Competition

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

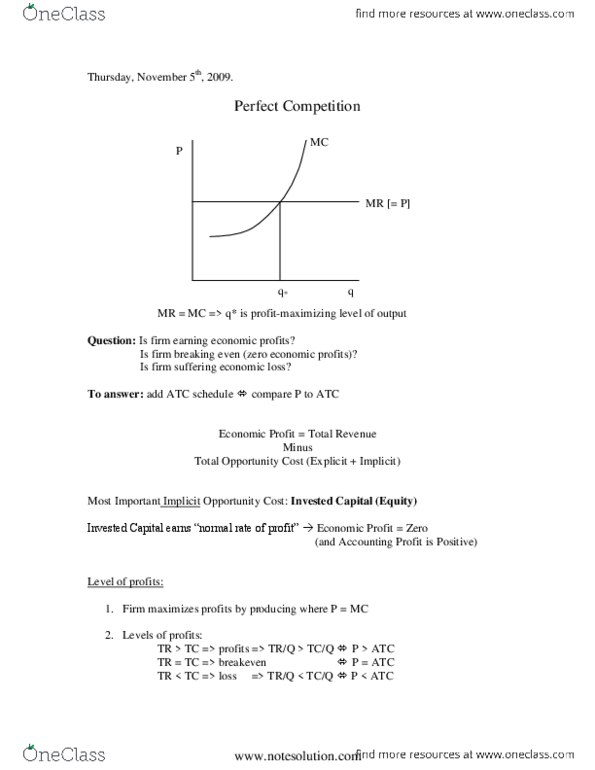

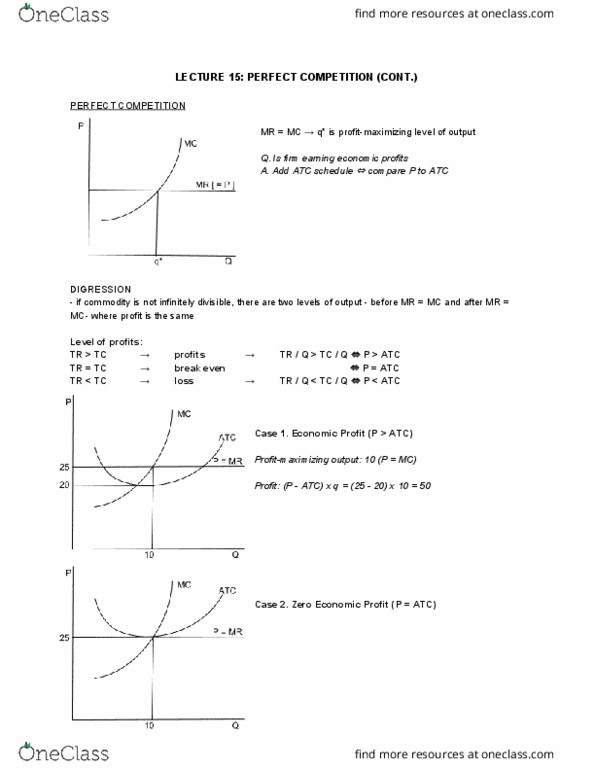

For any level of output, firm profits are given by: [p-atc(q)]q. Optimum profit: [p-atc(q*)]q: these are the maximum profits a firm can earn at price p. Break-even price: p = atc(q*) = mc(q*, this occurs at the minimum atc. The existence of profits or losses determines the long-run entry or exit decision of a firm in the industry: exit if profits are negative, stay/enter if profits are positive or zero. In the short run, firms can operate with a profit or loss. The magnitude of the loss will also affect short-run production decisions if p avc(q*), where the surplus can be applied to cover some fixed costs, part where atc > p, where fixed costs are uncovered . Input prices (wages) affects variable costs and marginal costs, and thus total costs.