ECO101H1 Lecture 22: Nov 20 - Monopolistic Competition

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

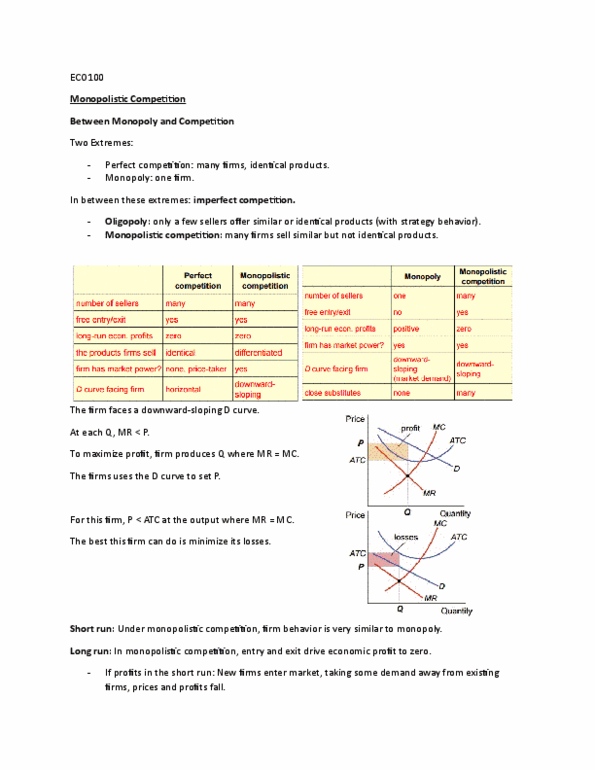

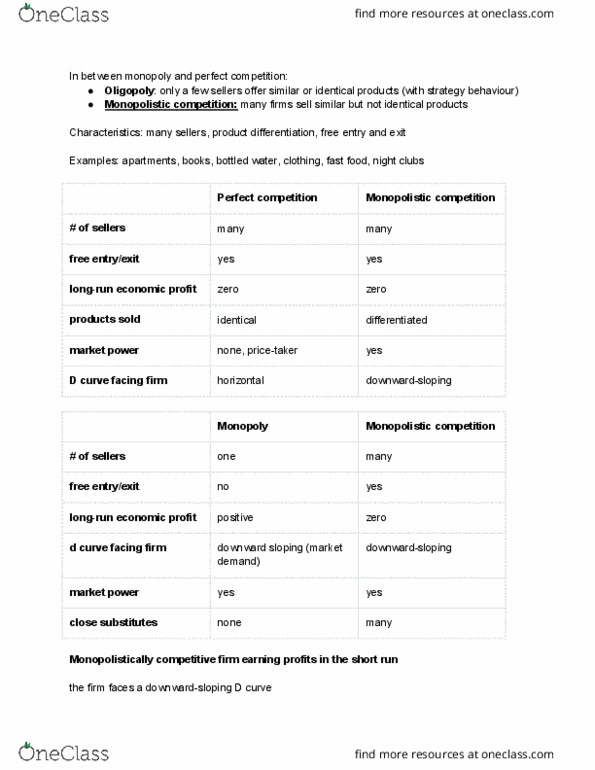

Perfectly competitive firm: price always equals the marginal cost of production, price equals average total cost. Because in the long run, entry and exit drive economic profit to zero. Monopoly: can use market power to keep prices above marginal cost. Positive economic profit for the firm and deadweight loss for society. Imperfect competition: industries that fall between cases of perfect competition and a monopoly, oligopoly. A market structure in which only a few sellers offer similar or identical products. Small number of sellers makes rigorous competition less likely and strategic interactions among them important. Economist"s measure a market"s domination by a small number of firms with a statistic called the concentration ratio. The percentage of total output in the market supplied by the four largest firms. Include industries such as breakfast cereal, aircraft manufacturing, household laundry equipment, cigarettes, etc: monopolistic competition. A market structure in which many firms sell products that are similar but not identical.