ECO101H1 Lecture Notes - Lecture 8: Monopoly Profit, Monopoly Price, Organic Food

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

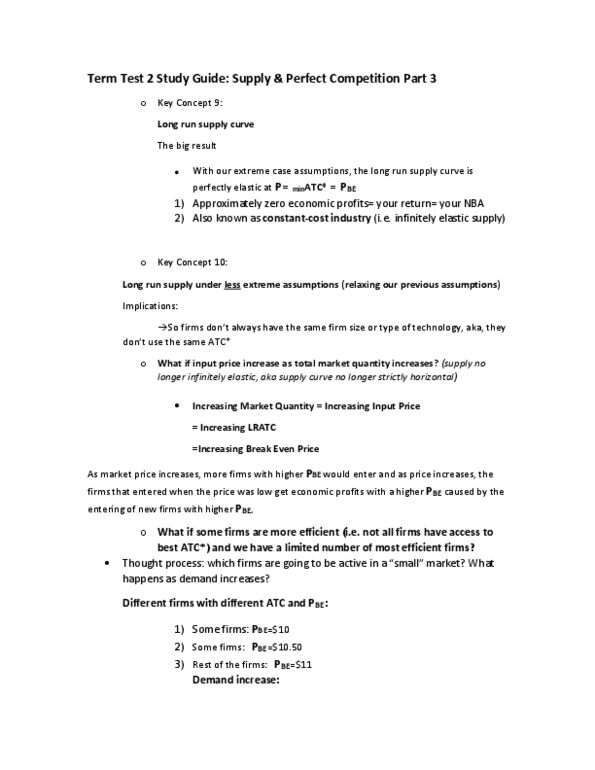

Demand increases, market price increases (from to ) Case 1: new firms have identical cost schedules as existing firms. 10,000 old firms and 1,000 new firms earn zero economic profits. Long-run industry supply curve is horizontal (perfectly elastic) Case 2: the entry of 1,000 new firms results in higher wages and mc of all firms increase by [so atc of all firms increase by ] In the long run, p==[minimum] atc of all firms. Price falls from short-term level () as new firms enter industry, but only to . In eco100, we will focus only on case 1. 1: as shown by case 2, we need to track how [minimum] atc changes as new firms enter industry to identify long-run industry supply curve. Single seller (of product with no close substitutes) Barriers to entry: legal barriers (legal monopoly) *one pipeline is efficient, the government won"t make 100 pipelines.