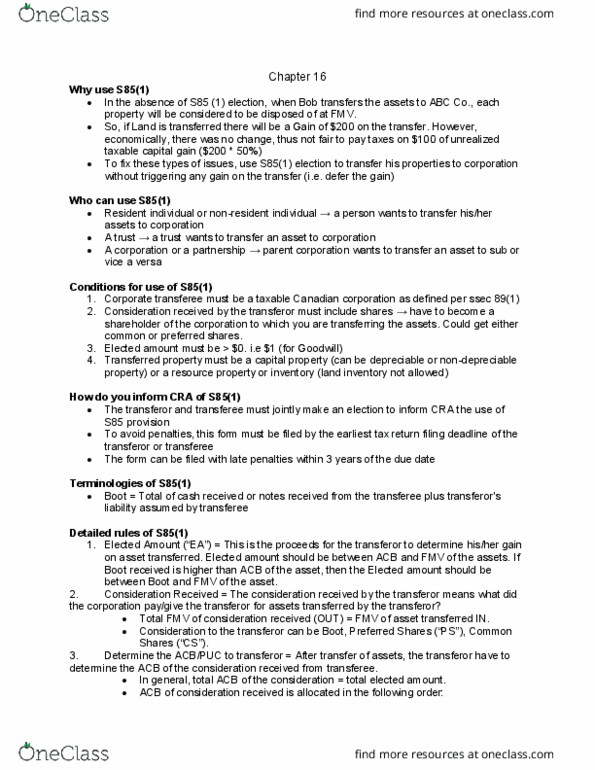

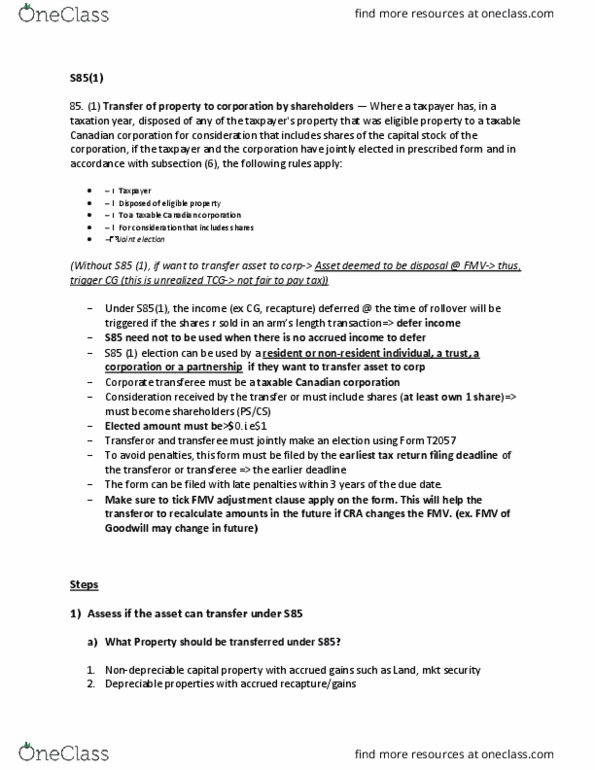

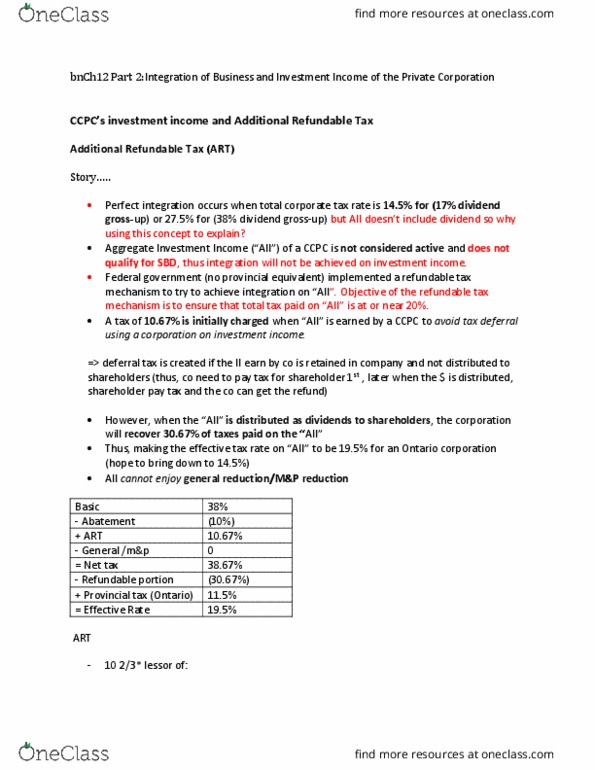

Tatiana partnership

The Tatiana Partnership is a calendar year, cash basis limitedpartnership which was formed on 1 January 2014. The partnership isin the business of training attack dogs and cats (business code541990). The address for the partnership and both partners is 300Montgomery Street, Suite 1050, San Francisco, CA 94104. Allbusiness is carried on in the San Francisco Bay Area, and thepartnership has no foreign activities of any kind. The partnershipreturn is filed in Ogden, Utah. The partnershipâs federal ID numberis 94-0070070.

The partnership agreement follows the provisions of IRC section704 and provides that gains, losses, and depreciation will beallocated in such a manner so as to account for the differencesbetween agreed market values and the tax basis of assetscontributed to the partnership. For example, should the agreedvalue exceed the tax basis of a contributed asset, any gain due tothe difference shall be allocated to the contributing partner uponsale of the asset. Any remaining gain shall be allocated in theâregularâ ratio in which partners share income and losses.Furthermore, depreciation expense on contributed assets is to beallocated to the noncontributing partner as if the assetâs FAIRMARKET VALUE were EQUAL to its tax basis; any remainingdepreciation is to be allocated to the contributing partner.

Outside of the special IRC Section 704 allocations discussed inthe preceding paragraph, all other items are allocated in theânormalâ profit and loss ratios for the partnership.

Data on the partners, the assets contributed by them, and theprofit and loss ratios agreed upon are as follows:

Tyr Slesnick (SSN; 007-06-1991), the general partner

Arekay Mitchell (SSN: 006-01-1985), the limited partner.

Tyr â 60% profit and loss ratio. Tyr contributed a parcel ofland (acquired on 1/1/1995 as investment property) and its relatedmortgage. The land originally cost $200,000 and had a fair marketvalue of $300,000 as of the date it was contributed to thepartnership. There was a $180,000 balance on the qualifiednonrecourse mortgage assumed by the partnership. The land is knownas âWhitaker Acresâ. The capital contribution of the land and itsrelated mortgage was made on the date the partnership was formed.The land was used by the Tatiana Partnership as a location to trainthe dogs.

Arekay â 40% profit and loss ratio. Arekay contributed a dogtraining machine valued at $80,000. The dog training machine wasacquired on 1/1/2009 at a cost of $120,000. The machine originallyhad a ten year life (5 years left@ 1/1/2014) and is depreciated onthe straight-line method using a 10 year life at the rate of$12,000 of depreciation per year. Accumulated depreciation of$60,000 ($120,000 cost less $60,000 accumulated depreciationthrough 12/31/2013) as of the date it was contributed to thepartnership.

The partnership keeps its books on the tax basis method withappropriate supporting schedules maintained to keep track of fairmarket value where required. Each partnerâs ownership of capital isper the books.

A. You need to make a journal entry to record Tyrâs capitalcontribution of the land subject ot the mortgage as of1/1/2014.

B. You need to make a journal entry to record Arekayâs capitalcontribution of the dog training machine as of 1/1/2014.

C. On 12/31/2014 (the last day of the year), the partnershippurchases a new piece of land (Darien Acres) for $4,500,000. The$4,500,000 purchase was 100% financed via a $1,000,000 RECORSE LOANfrom Union Bank and a $3,500,000 QUALIFIED NONRECOURSE FINANCINGfrom Wells Fargo bank. The recourse loan plus one yearâs interestat 10% is due in full on 12/31/2014, and no interest is payableuntil maturity. The qualified nonrecourse loan requires quarterlyinterest payments (at an 8% annual rate) with the first quarterlyinterest payment of $70,000 not being due until 3/31/2015 (i.e.,next year). This land will be used as a larger site on which totrain the dogs and cats â i.e., itâll be used as business land.

D. You need to record the depreciation expense on the dogtraining machine. Please note that the machine is deprecated usinga 10 year life for both regular and âalternative minimum taxâ.Depreciation. As noted in the facts, the machineâs tax depreciationis $12,000 ($120,000 original cost divided by 10 years). If themachineâs depreciation had been based on itâs $80,000 FMV, thedepreciation based on FMV would have been $16,000 ($80,000 FMVdivided by the 5 year remaining life). Youâre going to have tofigure out what to do and how to allocate the depreciation betweenthe partners.

E. The business purchased $920,000 of additional trainingequipment. This equipment was purchased on the day the partnershipwas formed, and it has been fully paid for as of the end of theyear. The partnership desires to claim the MAXIMUM depreciationallowed under the tax law, so youâll need to compute this andprepare a journal entry recording the depreciation. The propertywas purchased on 1/2/2013.

F. The property contributed by Tyr was known as âWhitakerAcresâ. This property was SOLD on July 4th of thecurrent year for $600,000 ($420,000 of cash is shown in a separateaccount, but no entry has been made to record the sale, so youâllneed to make the journal entry necessary to record the sale anddecide how to allocate the gain between the two partners.

REQUIRED:

1. Prepare journal entries to record the events listed in âAâthrough âFâ above. Label the entries âAâ through âFâ>

2. Post the journal entries to the cash activity and prepare aâworking trial balanceâ.