MGAB02H3 Lecture Notes - Lecture 2: Cash Flow, Irobot

10 May 2018

School

Department

Course

Professor

Straight line method SFP:

Depreciation : (Original cost - Residual Value)/Life

($ 40,000 - $ 10,000)/5 Cost

6,000 Acc Dep

Carry Value

Depreciation expense 6,000 Net Book value

Accumulated depreciation 6,000

Accelerated Method - Double Declining Method

Depreciation rate 100%/Life

Regular declining balance method - Depreciation Rate : 100%/5 = 20%

Double declining balance method - double the rate 20% x 2 = 40%

Usingh double declining. Depreciation :

Salvage value is not deducted up front

However, you can only depreciare up to the salvage value

Depreciation :

Carrying Value x Depreciation Rate

Year 1 : Carry Value

Depreciation : $ 40,000 x 40% 16,000 $ 40,000 - $ 16,000 = $ 24,000

Year 2 :

Depreciation : $ 24,000 x 40% 9,600 $ 24,000 - $ 9,600 = 14,400

Unit of output

Depreciation : (Cost - residual Value)/Total estimated output x output for the period

Car (Cost)_ 40,000

Residual Value 10,000

estimate mileage for the car 200,000 km

Year 1 - Drove 25,000 km

Depreciation - Year 1

Depreciation rate per output:

Cost 40,000

residual value 10,000

30,000

Total estimated output 200,000

Dep rate per km 0.15

depreciation for Year 1 $ 0.15 x 25,000 = 3,750

Activity 1:

Straight Line depreciation:

($ 3,000 - $ 500)/5 500

Double declining method:

Depreciation rate (non-double declining) 100%/5 20%

Double declining rate 40% (20% x 2)

Year 1 depreciation $ 3,000 x 40% = 1,200

Carrying Value - Year 1 $ 3,000 - $ 1,200 = 1,800

Year 2 depreciation $ 1,800 x 40% =- 720

Unit of Output method:

Depreciation rate per output:

($ 3,000 - $ 500)/6,000 = 0.4167

Year 2 depreciation:

0.4167 x 1,200 500

Every time the asset is disposed, I must record thegain or loss on disposal of assets

Disposal - selling ; Throwing it out; Trade in ; Insurance claim, etc

Gain or loss is claculated by comparing :

Recovery Value

vs

Carrying Value

Using Car example

Cost 40,000

residual value 10,000

Life 5 years

Sold car at end of year 2 for $ 30,000

At end of Year 2,

Carrying Value Accumulate depreciation

Cost 40,000 Cash

Acc depreciation (2 years) 12,000 Gain on dispsoal of car

Carrying Value 28,000 Car

recovery Value 30,000

Gain on dispsoal 2,000

Activity 4:

Trade In Value 3,000 ($ 10,000 - $ 7,000)

Carrying Value (irobot - Yr 4) 1,000 ($ 3,000 - ($ 500 x 4))

Gain on trade in 2,000

Disposal of old New

Trade In Value 3,000 I-robot

Accumulated Depreciation 2,000 Cash

Cost of irobot 3,000 Trade in value

Gain on disposal of old 2,000

Change in estimate (Residual value or life)

Every time when these change, depreciation going forward will need to change

To do the new depreciation

- Calculate the carrying value of the asset

- Assume using straight line, new depreciation = (Carrying value - revsied residual value)/remaining useful life

Car example - above

Assume at the end of year 2 - change the residual value to $ 5,000; adding 2 additional years to the life

Assume we use straight line depreciation

Depreciation per year from Year 3:

carrying value at end of year 2 :

Cost 40,000

Accumulated depreciation 12,000 ($ 40,000 - $ 10,000)/5 x 2

carrying value at end of year 2 : 28,000

Revised depreciation

Carrying value (end of yr2) 28,000

Revised residual value 5,000

23,000

Remaining Life 5 (5 years - depreciated 2 years + 2 years)

Revised depreciation per year 4,600

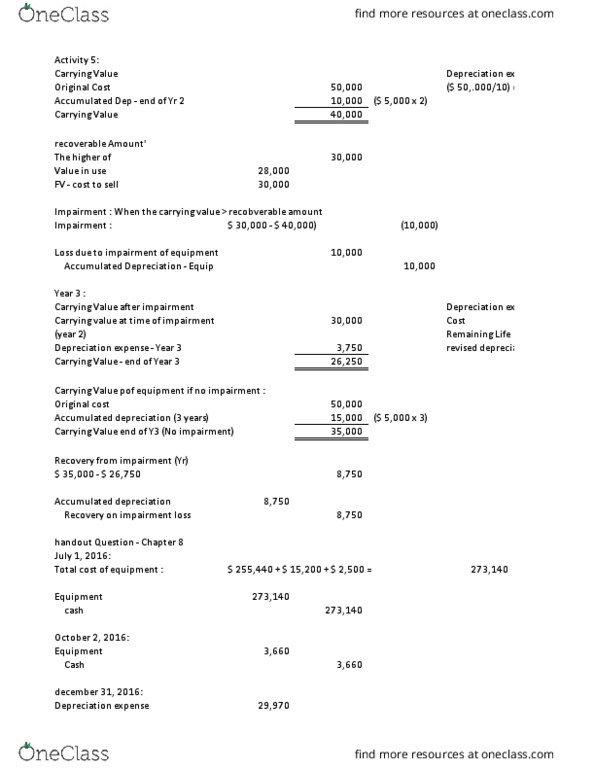

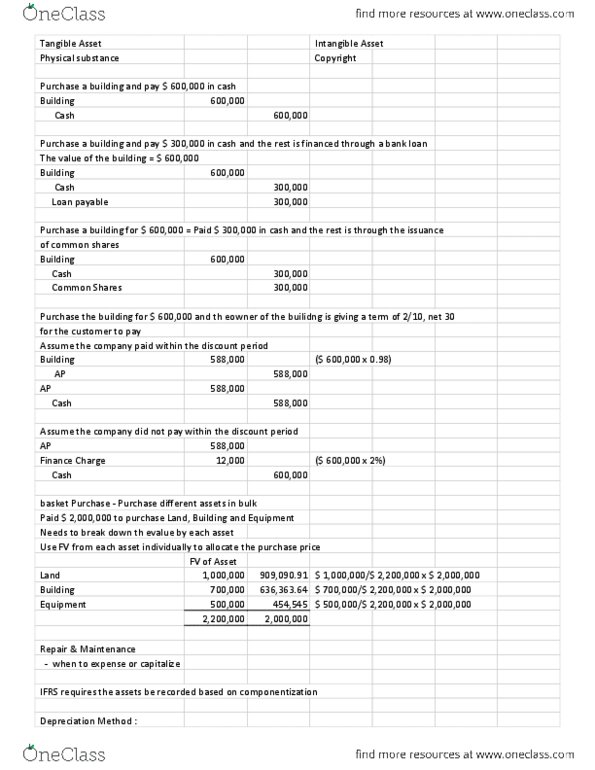

Problem 8-2

January 2:

Machine 81,400

Common Shares 7,000 ($ 3.50 x 2,000)

Notes Payable 45,000

Accounts Payable 29,400 ($ 82,000 - $ 7,000 - $ 45,000) x 98%

Machine 2,400

Cash 2,400

Clean up expense 100

Cash 100

January 15:

Accounts Payable 29,400

Discount Lost 600

Cash 30,000

April 16:

Notes Payable 45,000

Interest expense 1,500 $ 45,000 x 8%/12 x 3.5

cash 46,500

Document Summary

Depreciation : (original cost - residual value)/life ($ 40,000 - $ 10,000)/5. Regular declining balance method - depreciation rate : Double declining balance method - double the rate. However, you can only depreciare up to the salvage value. Depreciation : (cost - residual value)/total estimated output x output for the period. Straight line depreciation: ($ 3,000 - $ 500)/5. Depreciation rate per output: ($ 3,000 - $ 500)/6,000 = Every time the asset is disposed, i must record thegain or loss on disposal of assets. Disposal - selling ; throwing it out; trade in ; insurance claim, etc. Gain or loss is claculated by comparing : Sold car at end of year 2 for $ 30,000. Every time when these change, depreciation going forward will need to change. Calculate the carrying value of the asset. Assume using straight line, new depreciation = (carrying value - revsied residual value)/remaining useful li.