MGT120H5 Lecture Notes - Lecture 9: Cash Flow, Grocery Store, Decision Aids

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

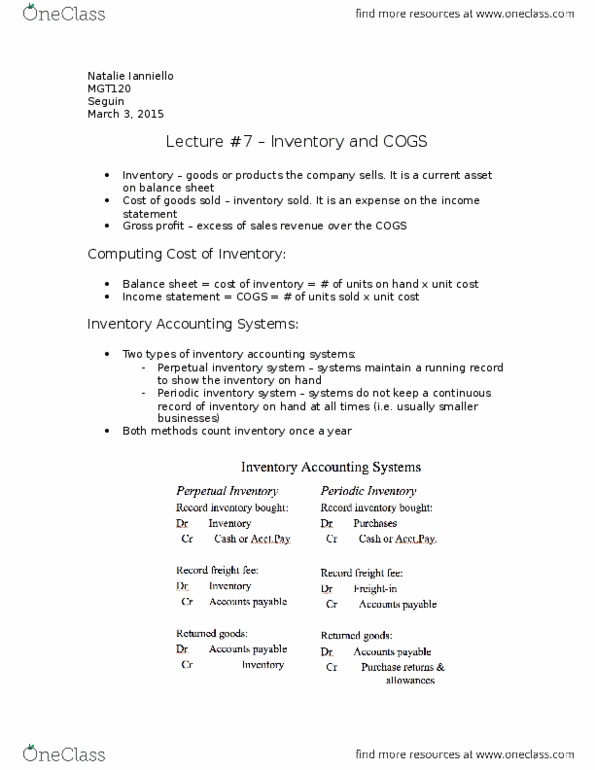

Week 9 march 1 (week 7: midterm; week 8: reading week) Chapter 6 inventory and cost of goods sold. Accounts receivable: estimating bad debts allowance method: Writing off and recovery of accounts receivable. Ratios: current, acid-test, and days" sales in a/r. Review question: accounts receivable has a debit balance of ,300, and allowance for. Uncollectible accounts has a credit balance of sh. ,300-200 = 2,100 (ar balance after credit allowance) (2,300-80) (200-80) = 2,100: no affect of net receivable (same number either way) The goods/products the company sells: current asset on balance sheet. Computing the cost of inventory: balance sheet. Cost of inventory on hand = number of units on hand x unit cost. Cost of goods sold = number of units. Accounting for inventory sold x unit cost: 2 main types of inventory accounting systems: 1) perpetual inventory system (more expensive, most used by businesses) Systems maintain a running record to show the inventory on hand at all times.