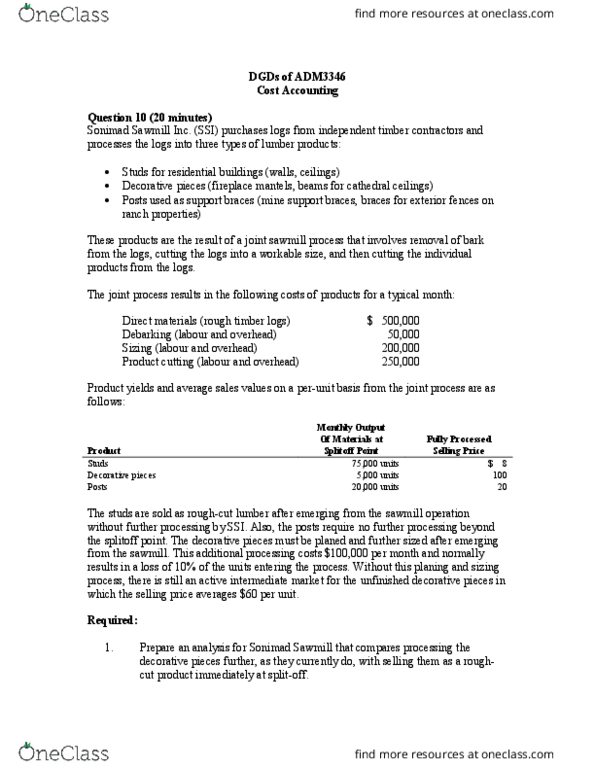

ADM 3346 Lecture Notes - Lecture 7: Earnings Before Interest And Taxes, Gross Margin, North Rhine-Westphalia

Document Summary

Get access

Related Documents

Related Questions

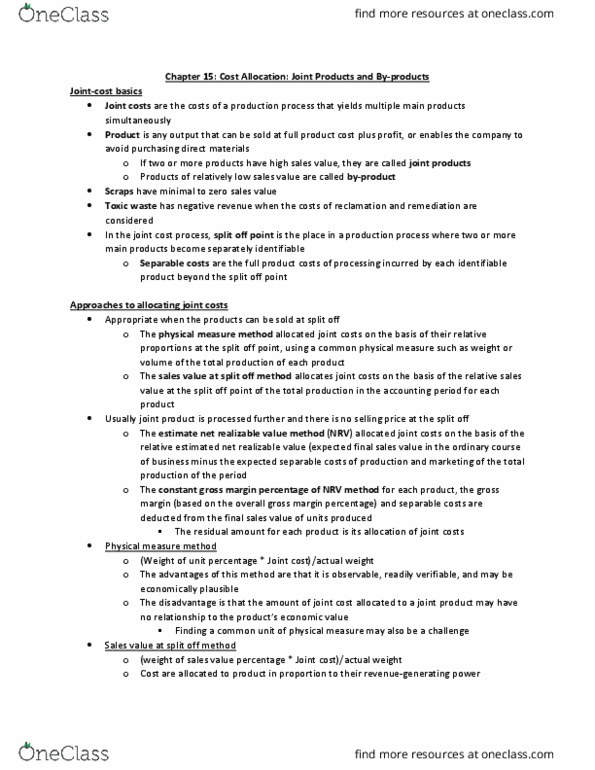

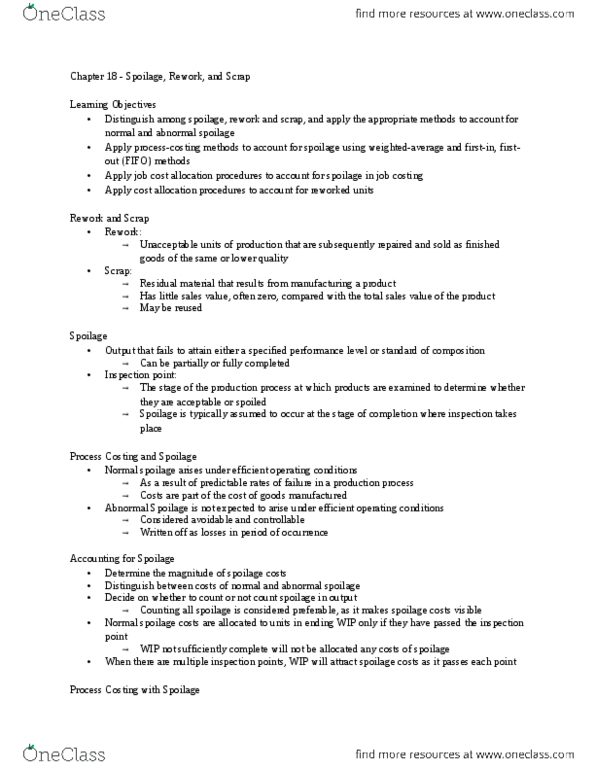

Joint Cost Allocation

Your firm pays for mineral rights at the Lego Mine, which contains diamonds, citrine, rubies, and emeralds, as well as large quantities of plain rock. Your firm uses the stones that are mined for the following products:

| Diamond rings | 2 |

| Citrine bracelets | 2 |

| Ruby bracelets | 2 |

| Emerald rings | 3 |

| Bags of rock |

A ring needs 4 stones.

A bracelet needs 10 stones.

Your firm has two kinds of employees: miners and jewelers. Miners go through the rocks in the mine, sort the diamonds, citrine, rubies, emeralds into individual transportation containers, and bag up the plain rock for sale landscapers. The transportation containers are then sent on to the jewelers, who make rings and bracelets.

Go through one production period, and keep track of times for the following:

Mining: 36 seconds

Making diamond rings: 12.5 seconds

Making citrine bracelets: 12.5 seconds

Making ruby bracelets: 12.5 seconds

Making emerald rings: 12.5 seconds

After all products are manufactured and ready for sale, complete the requirements below. Plain rock is treated as a byproduct. Plain rock are 20 stones. Calculate following costs were incurred this period:

| Cost of mineral rights | $2000 |

| Company overhead | $1500 |

| Mining labor, paid at $5/second | |

| Jeweler labor, paid at $10/second | |

| Bracelet settings at $100/bracelet | |

| Ring settings at $50/ring |

Bags of rock sell for $100 at splitoff. The following are per-unit prices your firm charges for each jewelry product, as well as how much each individual stone could sell for (at splitoff):

| Per ring or bracelet | Per stone | |

| Diamond | $1000 | $400 |

| Citrine | $500 | $100 |

| Ruby | $700 | $175 |

| Emerald | $800 | $200 |

1. Calculate total joint costs, separable costs for each product, and NRV for each product

2. Calculate the allocated joint costs and the profitability of each product line under each of the following assumptions:

a. The byproduct is accounted for at the time of sale, and sales value at the splitoff point is the allocation base for joint costs

b. The byproduct is accounted for at the time of production, and NRV is the allocation base for joint cost

c. The byproduct is accounted for at the time of production, and number of stones is the allocation base for joint cost

3. Briefly, state which cost allocation base is the most appropriate for this company, and explain why.