ADM 2341 Lecture 6: Chapter 8- Absorption Costing

10 Nov 2015

School

Department

Course

Professor

Document Summary

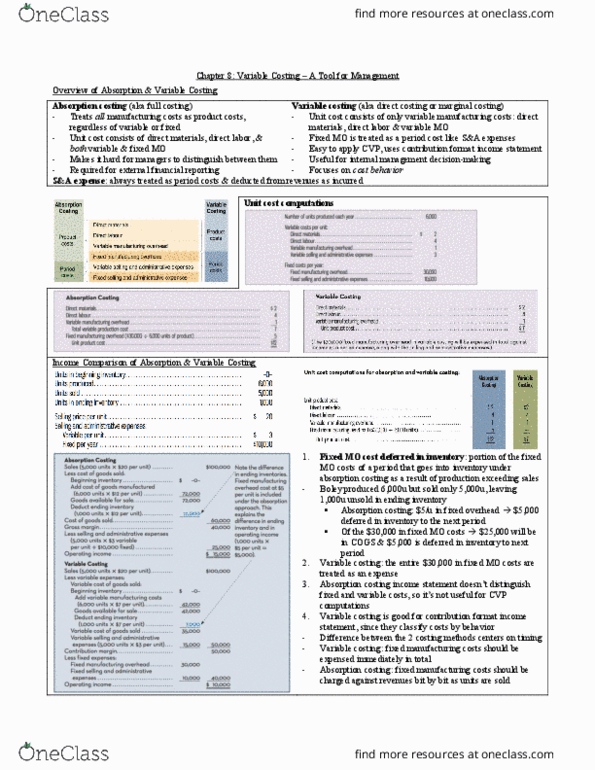

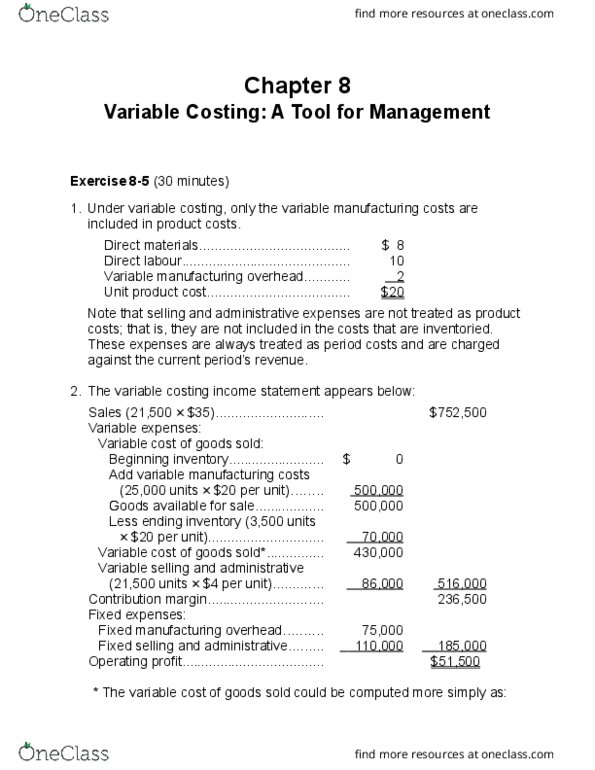

Harvey company produces a single product with the following information available: Under absorption costing, selling and administrative expenses are always treated as period expenses and deducted from revenue as incurred. We can reconcile the difference between absorption and variable costing by: We can reconcile the difference between absorption and variable income as follows: Effect of changes in production on operating income: In a previous example, 25,000 units were produced each year, but sales increased from 20,000 units in year one to 30,000 units in year two. In this revised example, production will differ each year while sales will remain constant. Effect of changes in production: harvey company year two. Net operating income is not affected by changes in production using variable costing. Net operating income is affected by changes in production using absorption costing even though the number of units sold is the same each year.