ADM 2341 Lecture Notes - Lecture 3: Finished Good

22 Apr 2018

School

Department

Course

Professor

Document Summary

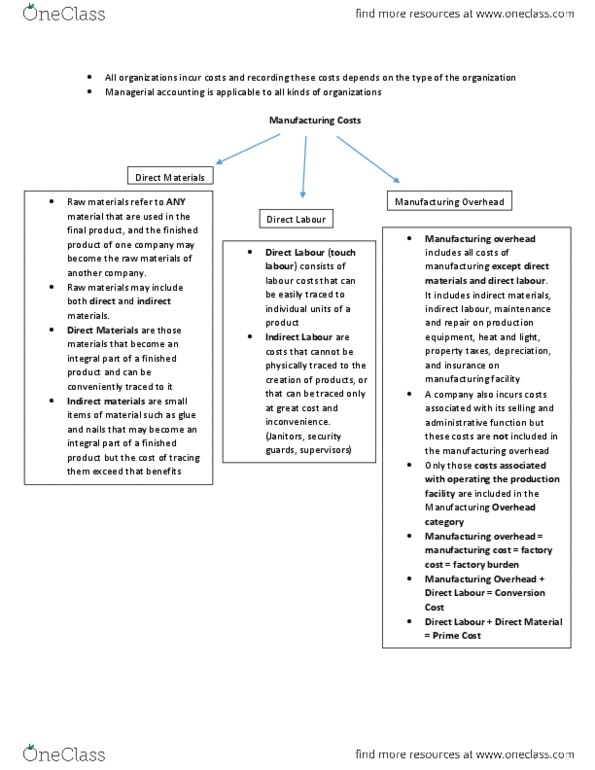

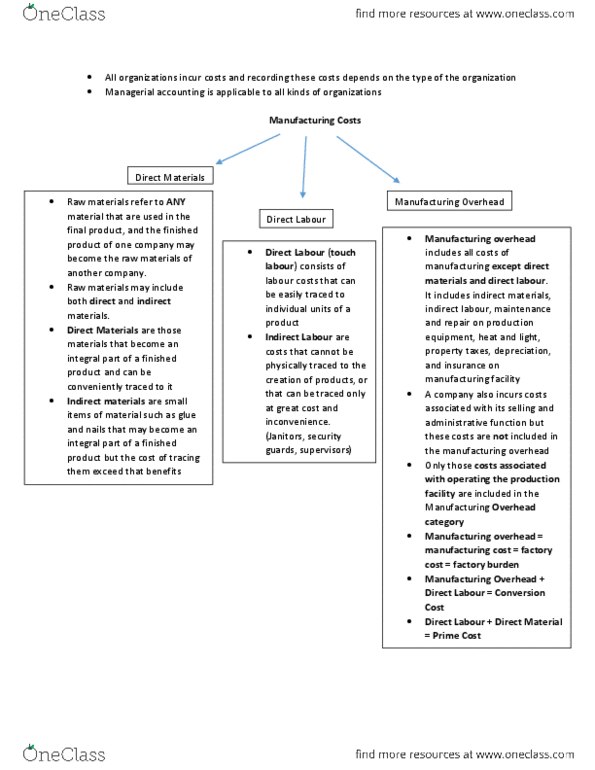

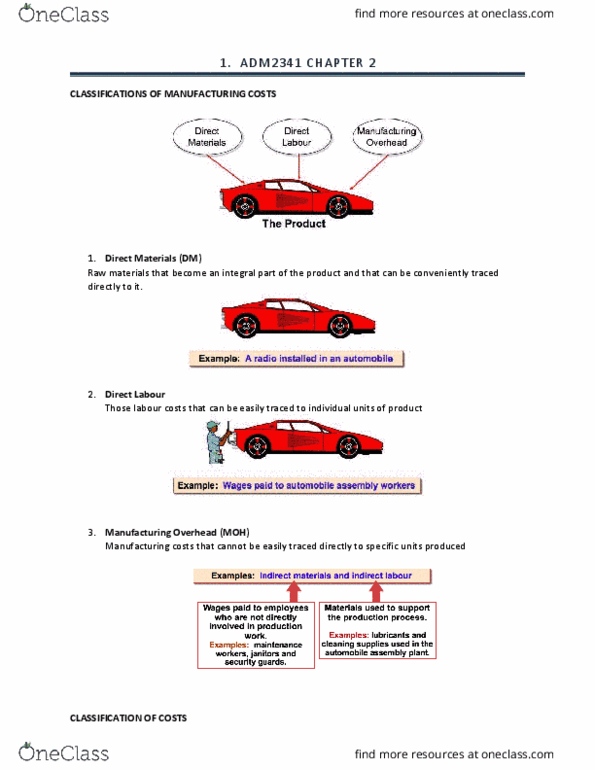

> process cost systems = apply costs to similar products that are mass-produced in a continuous way (pop, oli, chemicals) > job-order cost system = costs are assigned to a specific job (e. g, construction of a customized home, the making of a motion picture, or the manufacturing of a specialized machine) >both costing systems track three manufacturing cost elements direct materials, direct labour, and manufacturing overhead: the accumulation of the costs of materials, labour, and overhead. > in both costing systems, raw materials are debited to raw. Materials inventory, factory labour is debited to factory labour, and manufacturing overhead costs are debited to manufacturing. >as noted above, all manufacturing costs are accumulated by debits to raw materials inventory, factory. These costs are then assigned to the same accounts in both costing systems work in. Process, finished goods inventory, and cost of goods sold. The methods of assigning costs, however, differ significantly. Diff: the number of work in process accounts used.