ADM 1340 Lecture Notes - Lecture 5: Gross Profit, Gross Margin, Uptodate

26 Apr 2017

School

Department

Course

Professor

42

ADM 1340 Full Course Notes

Verified Note

42 documents

Document Summary

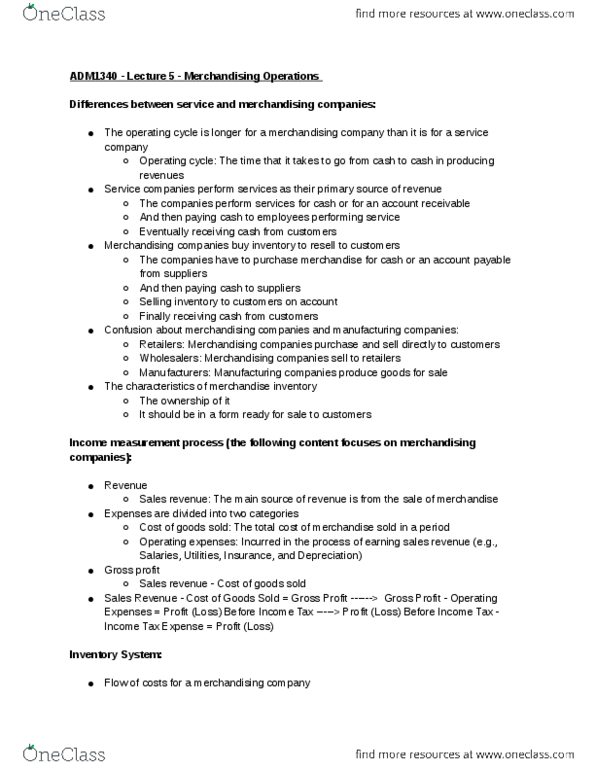

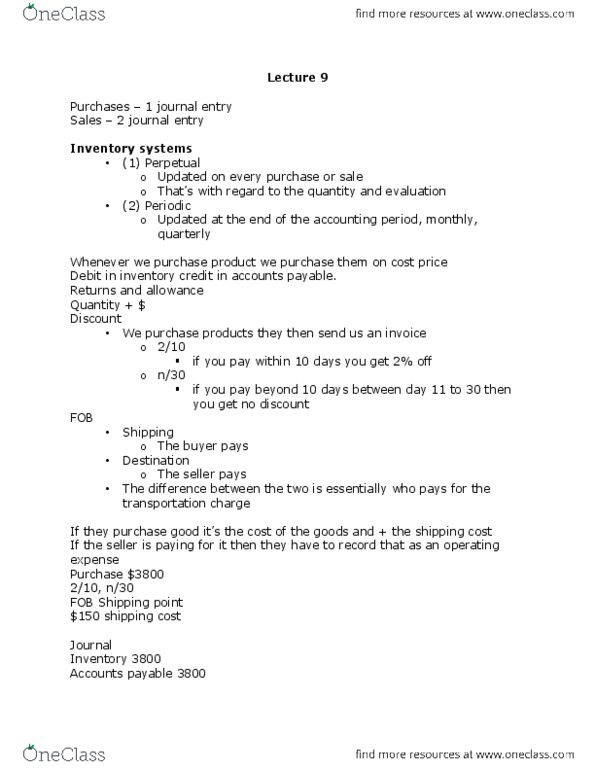

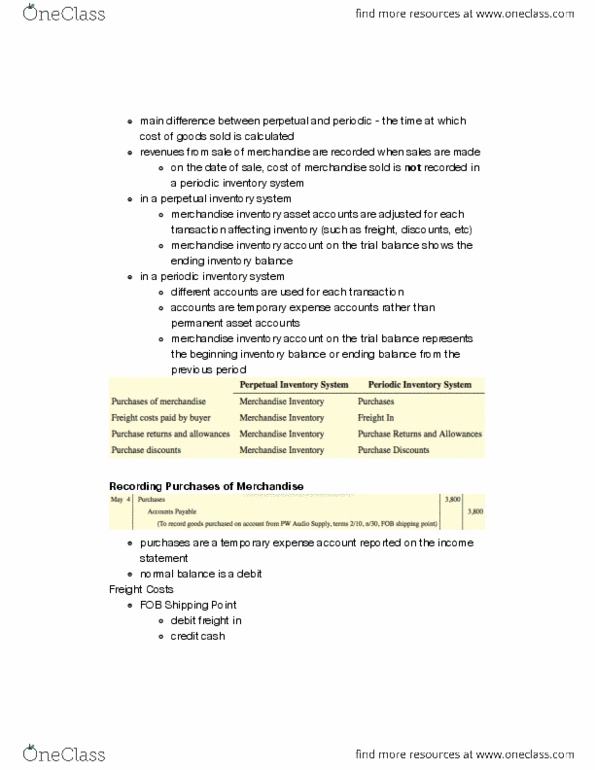

Merchandising involves purchasing products (inventory) to resell to customers. A merchandising company keeps track of its inventory to determine what is available for sale (inventory) and what has been sold (cost of goods sold) Two systems to account for inventory: perpetual , periodic , perpetual, detailed records of the cost of each inventory purchase and sale are maintained , cost of goods sold is determined each time a sale occurs. Cash or a/p: gst, pst, hst, do not form part of the cost of the merchandise, freight costs , costs of transporting the goods to the (cid:271)uyers" pla(cid:272)e of (cid:271)usiness, freight terms state who pays the freight charges. No journal entry for the seller: purchase returns and allowances. Purchase return: the buyer returns the goods to the seller and receives a cash refund or credit. Purchase allowance : the seller gives an allowance (deduction ) from the purchase price.