BUSI 2160U Lecture Notes - Lecture 5: Financial Statement, Income Statement, Equity Method

Document Summary

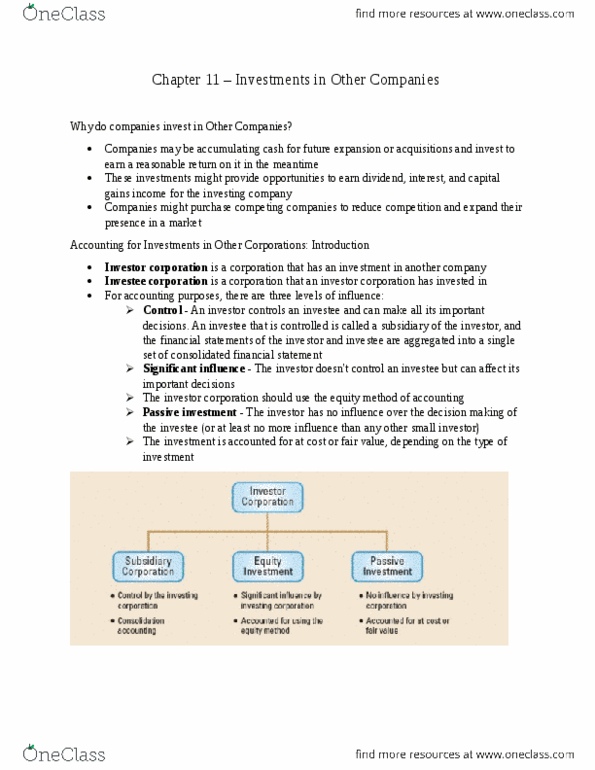

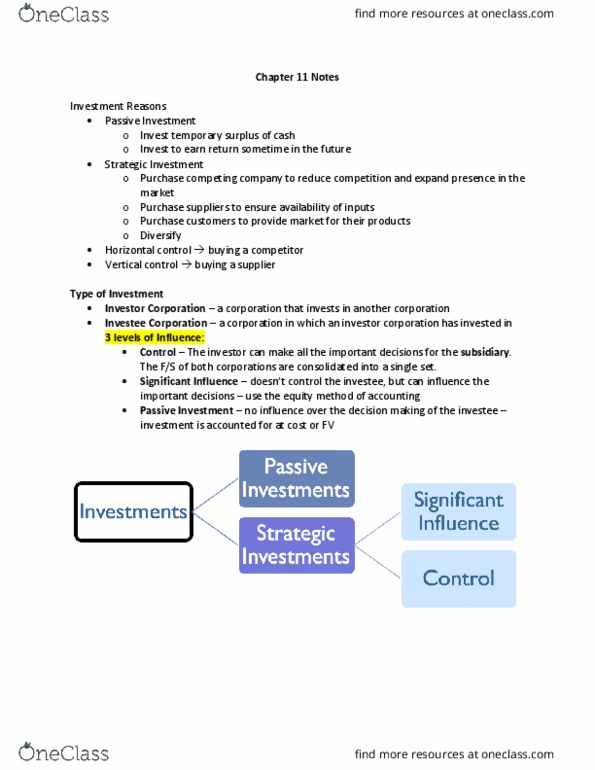

Use of excess cash: typically, short term investment. Investor can make all important decision (consolidated financial statements) Investor can affect a number of important decision (equity method) Investor has no influence over decisions (cost or fair value) Provide users information on the group of companies (big picture) The entities are separate legal entities and must file individual tax returns. Assets and liabilities may be valued differently. Cost to parent must be allocated: fair value if identifiable net assets acquired, any excess purchase price is goodwill. 1st transaction: investor (parent) acquires control of the investee (subsidiary) The investment is recorded in the books of the parent at its cost. The price paid for subsidiary will be different than the amount of the book values on the books of subsidiary. Date of acquisition: consolidated balance sheet includes: Goodwill, if any, recorded: does not include: