SCMA*2000 Lecture Notes - Lecture 31: Finished Good, Total Absorption Costing, Earnings Before Interest And Taxes

Document Summary

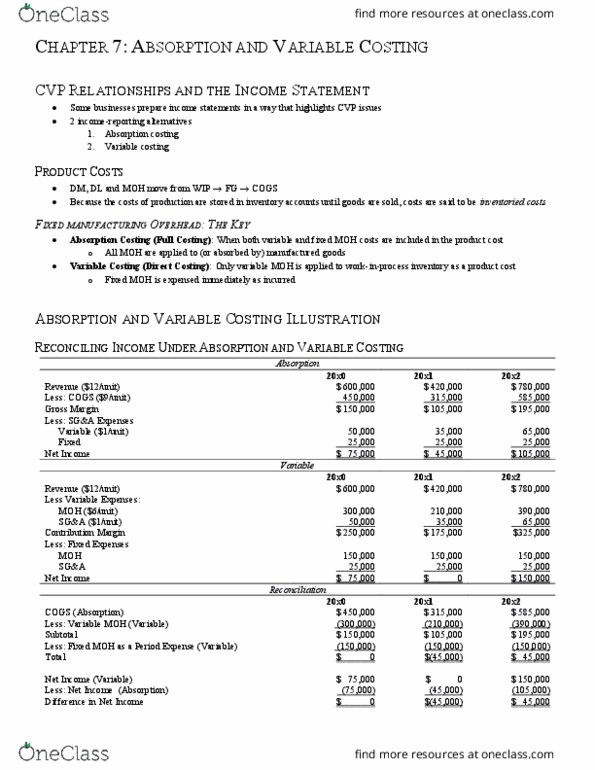

Management has decided to run its factory at capacity, producing 25,000 units/year, regardless of demand. Year 1 production = sales = 25,000 units. Year 2 production = 25,000 units > sales = 20,000 units. Under absorption costing, ,000 of moh cost are located on the balance sheet under. Under variable costing, that ,000 is located on the income. Add fixed moh deferred in finished goods inventory. Year 3 production = 25,000 units < sales = 30,000 units. Add cost of goods man. ( x 25,000) Add cost of goods man. ( x 25,000) Under absorption costing, ,000 of moh cost that was located on the balance sheet under. Finished goods inventory have moved onto the income statement as part of the cost of. Less fixed moh transferred in finished goods inventory. Assuming the company uses absorption costing: a) b) Assuming the company uses variable costing: a) b) Reconcile any difference that may exit between the absorption and variable income.