COMM 455 Lecture Notes - Lecture 8: Income Statement, Write-Off

Document Summary

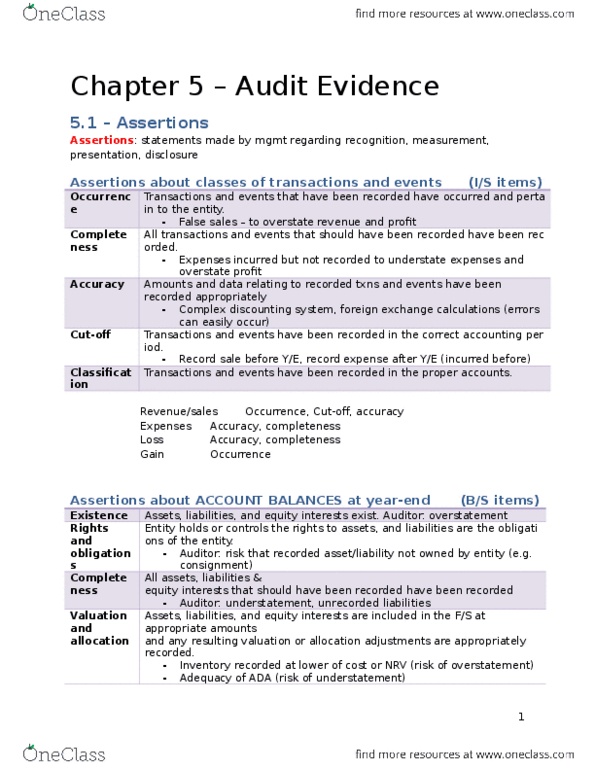

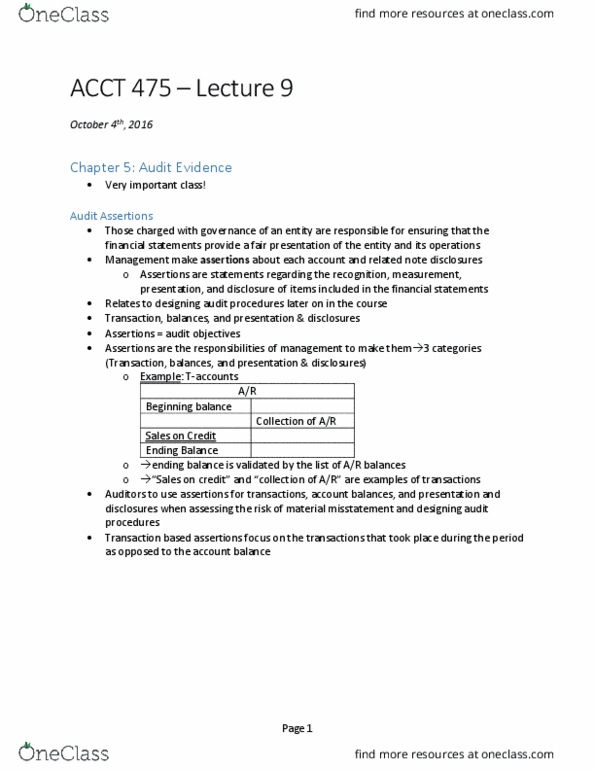

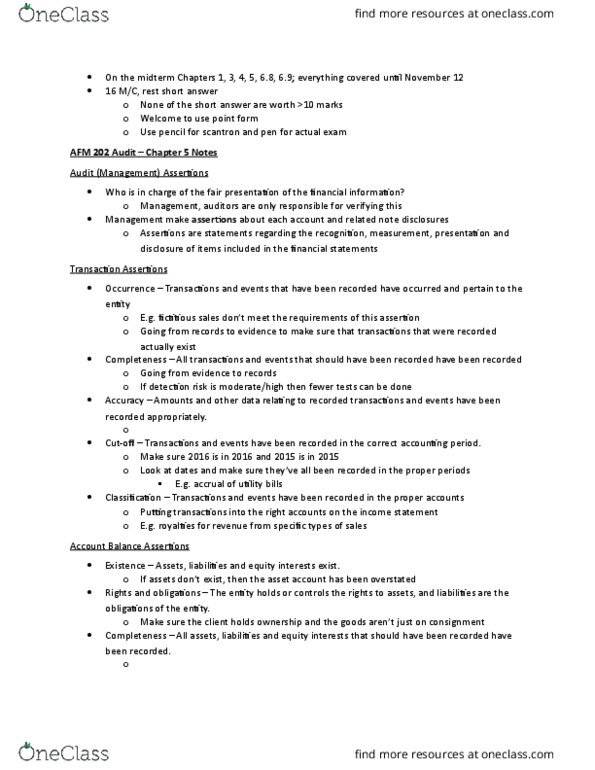

Chapter 5 assertions: most important for cpa. Class of transaction (revenue, expense - properly record, then happy with income statement) (completeness, occurrence, cutoff, classification, accuracy) e. g. revenue risk it is overstated. Completeness: all transactions taken place have been accounted for. Accuracy: transactions have been recorded appropriately underlying data (gst) is accurate: e. g. Controls tested: take sample prices entered correctly, invoices as evidence, classified in right account. Classification: transactions have been recorded in the proper accounts: revenue usually only one account, sales commission is dependent on where sales are made. Make sure alberta is alberta (no sales tax), bc is bc: purchases more accounts. Cutoff: transactions and events have been recorded in proper accounting period revenue: bring sales of next period into current, recognised too early overstate, minimize tax push to next period, pay less tax. Account balances (assets and liability) 4 assertions; e. g. inventory. E. g. precious metals risk in area: inventory count, additions important.