MTHEL131 Lecture 11: MTHEL-L11

20 Jan 2020

School

Department

Course

Professor

Document Summary

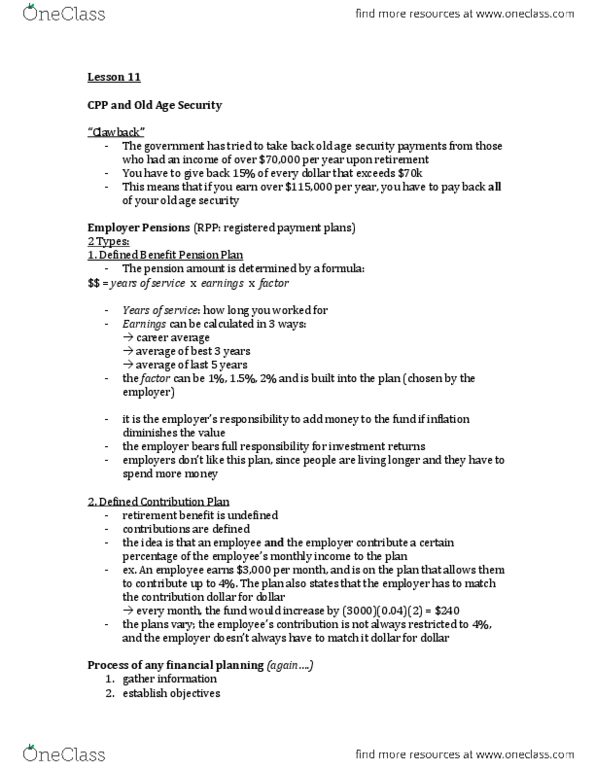

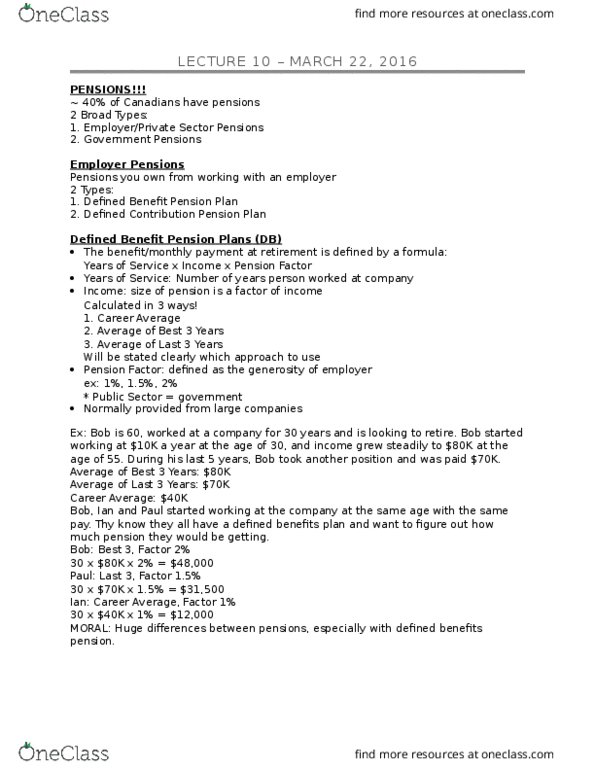

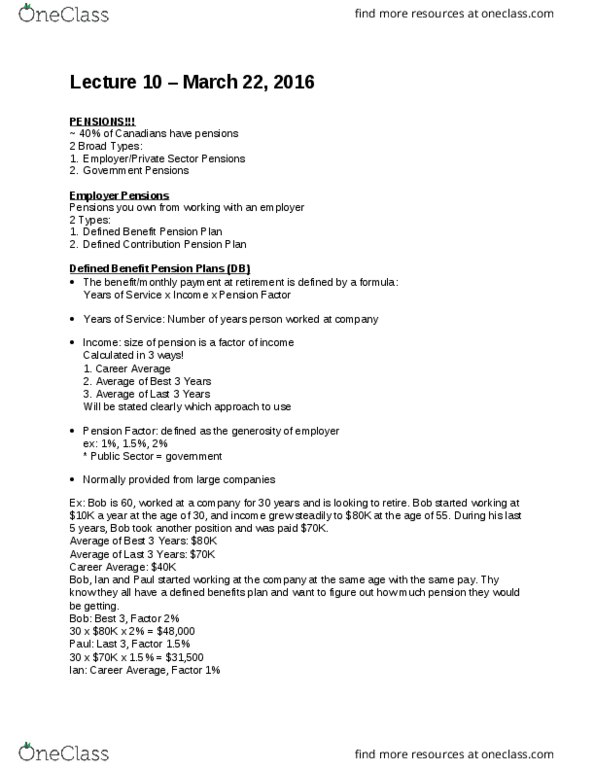

If the stock market drops/crashes (significantly) before the owner of the pension"s retirement is not effected. If the investment fund of a person is doing poorly, it is the employer"s responsibility. Longevity investment (people living longer than expected) Employee is asked to contribute up to 3% of gross earnings (income) If their income is /mo, they would contribute /mo which is optional and the money is matched by employer. (matched dollar for dollar) So the fund gets per month and is invested. Employer does not take on the longevity and investment risks. No longevity risk and investment risk for employer. Only 32% take advantage of the maximum matching. They should take advantage asap since it is matched (double money) For defined contribution plans, if you worked for that company at least 2 years, the employer contributions become. Vested and can not be taken back and if that employee leaves they take everything and the investment returns.