AFM391 Lecture Notes - Lecture 5: Stax Records

28 Jun 2018

School

Department

Course

Professor

These collective obligations are referred to as multiple deliverables

○

The liability recognized should reflect the portion of the transaction price allocated to the

future performance obligation. Transaction price is allocated based on the relative

observable stand

-

alone sales price of the performance obligations

○

If the stand-alone selling price is not directly observable, the estimate should factor the

likelihood that the option to the material right might not be exercised

○

Transaction price be adjusted to incorporate the effects of the time value of money if the

contract includes a significant financing component, but customer loyalty programs are

exempt from this requirement

○

Factors to be considered when determining the amount of the liability to be recognized for

unsatisfied (means haven't performed yet, not meaning bad performances for customers)

performance obligations include:

•

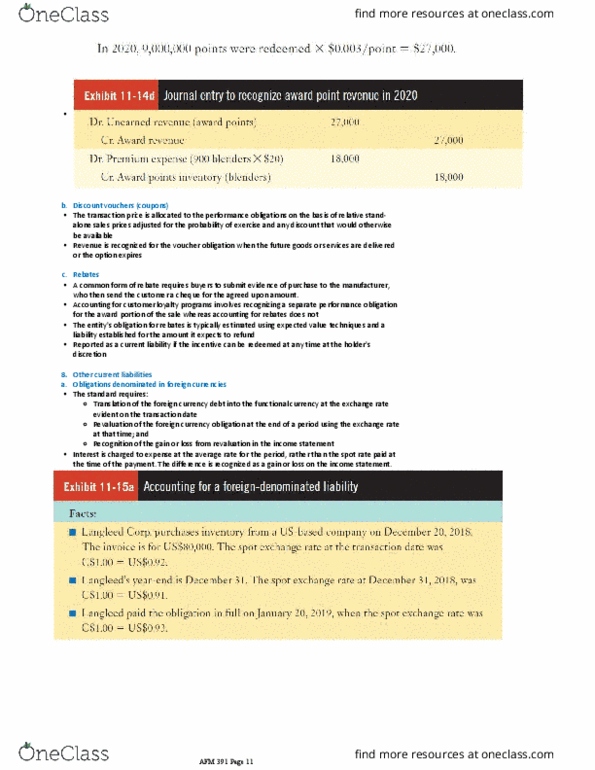

Awards supplied by the entity: the transaction price must be allocated to the performance

obligation in accordance with the guidance in IFRS 15. see exhibit 11

-

13 and 11

-

14

○

Third party awards:

the enterprise records the full transaction price as revenue at the time

of sale. The enterprise contemporaneously recognizes an expense for the cost of purchasing

the points from the third party. The reporting entity has satisfied both performance

obligations

○

Choice of awards:

ignored.

○

Once the stand

-

alone value of the performance obligations has been estimated, the journal

entry to record the sale can be made

○

○

The hotel expects 40,000 points to be redeemed so the value per points is $50,000/ 40,000

points = $1.25/point

○

In 2019, 30,000 x $1.25 = $37,500.00 $37,500

○

○

○

The accounting for loyalty programs differs depending on who supplies the awards

•

AFM 391 Page 9

Document Summary

These collective obligations are referred to as multiple deliverables. Factors to be considered when determining the amount of the liability to be recognized for unsatisfied (means haven"t performed yet, not meaning bad performances for customers) performance obligations include: The liability recognized should reflect the portion of the transaction price allocated to the future performance obligation. Transaction price is allocated based on the relative observable stand-alone sales price of the performance obligations. If the stand-alone selling price is not directly observable, the estimate should factor the likelihood that the option to the material right might not be exercised. Transaction price be adjusted to incorporate the effects of the time value of money if the contract includes a significant financing component, but customer loyalty programs are exempt from this requirement. The accounting for loyalty programs differs depending on who supplies the awards.