AFM363 Lecture Notes - Lecture 13: Fruit Tree, Capital Gain, Working Capital

23 Jun 2020

School

Department

Course

Professor

Document Summary

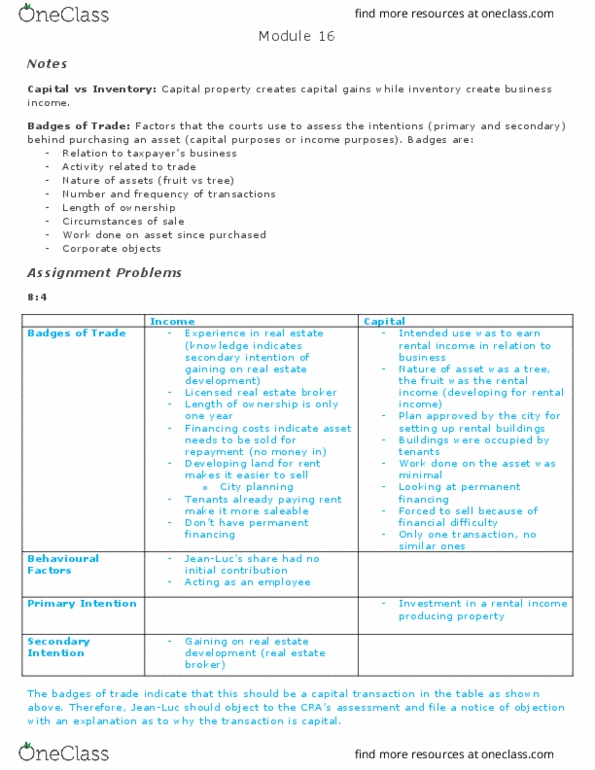

Realize capital gains when you dispose of capital property, taxpayers prefer capital gains, 50% inclusion rate, cra prefers income treatment, prefer capital loss. How to assess: capital property, depreciable property, disposition is capital gain or loss. Inventory: relevant in computing business income, badges of trade. Intention at time of purchase: facts and circumstances. Facts leading up to, during and after the transaction: behavioural factors, badges of trade, balanced analysis. Strengths and weaknesses of argument: advise clients of risk, arrive at a conclusion. Badges of trade: relation of transaction to taxpayer"s business, activity normally related to trade, nature of assets, fruit vs tree analogy, fixed assets, capital gains. Fruit tree, capital property: care for it, will sell fruit on the tree, value when matured, working capital assets, income. Fruit provides steady stream of income every year. Supplement work done on asset since purchase: number and frequency of transactions, circumstances that cause the sale, corporate objects or partnership agreement.