AFM291 Lecture Notes - Lecture 10: Systematic Risk, Risk Premium, Capital Asset Pricing Model

11 Sep 2017

School

Department

Course

Professor

Document Summary

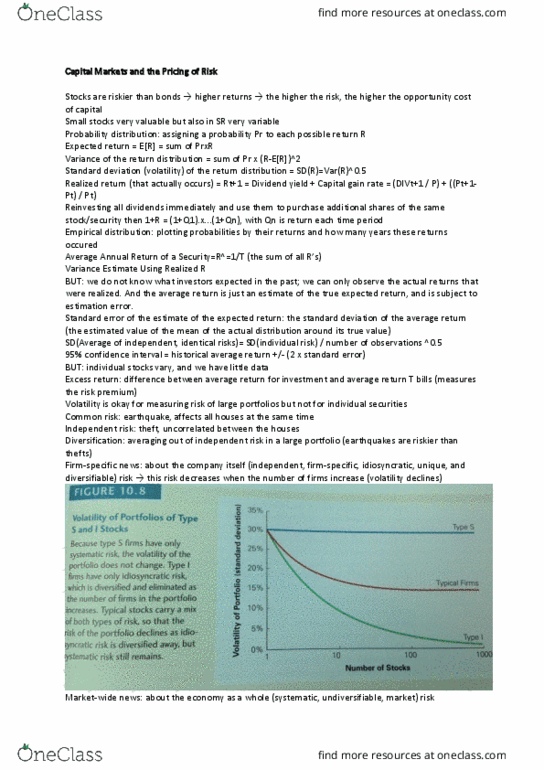

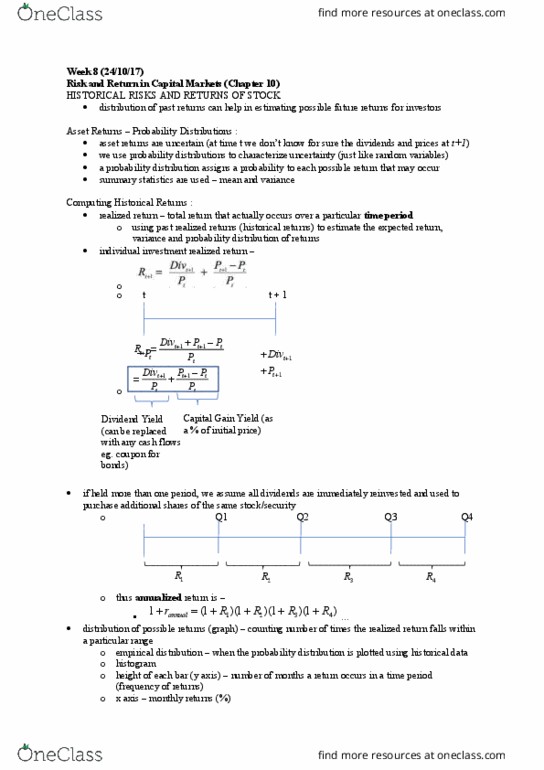

Afm 273 chapter 10: capital markets and the pricing of risk. Probability distributions - when an investment is risky, there are different returns it may earn. Each possible return has some likelihood of occurring. Expected (mean) return - calculated as a weighted average of the possible returns, where the weights correspond to the probabilities. Variance the expected squared deviation from the mean. Standard deviation the square root of the variance. Both are measures of the risk of a probability distribution. In finance, the standard deviation of a return is also the volatility. Realized return the return that actually occurs over a particular time period. If you hold the stock beyond the date of the first dividend, then to compute your return you must specify how you invest any dividends you receive in the interim. Let"s assume that all dividends are immediately reinvested and used to purchase additional shares of the same stock or security.