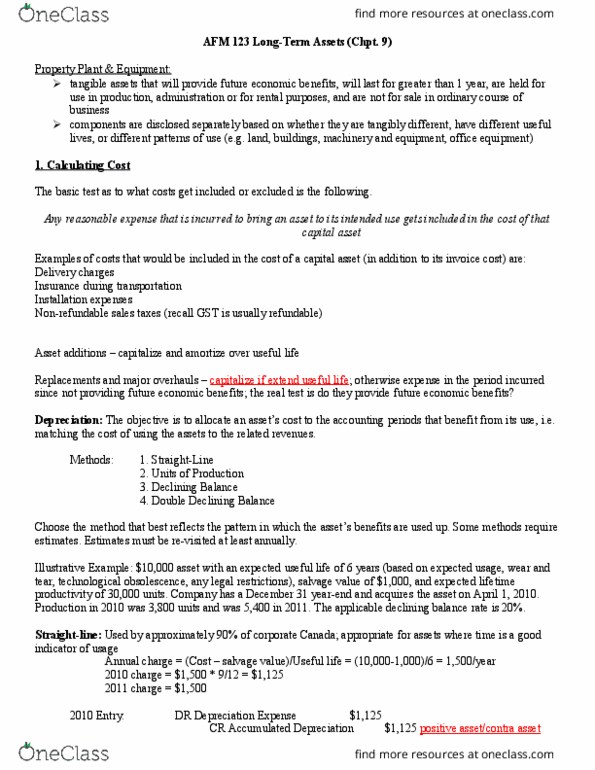

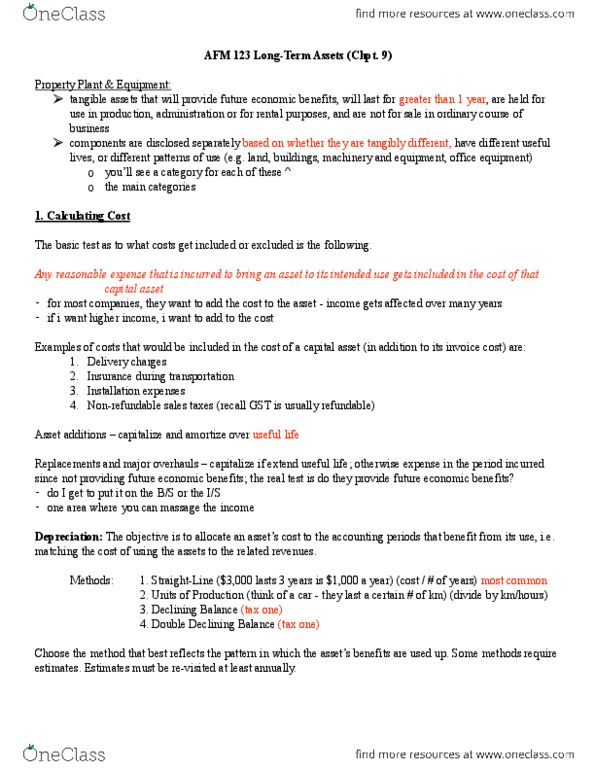

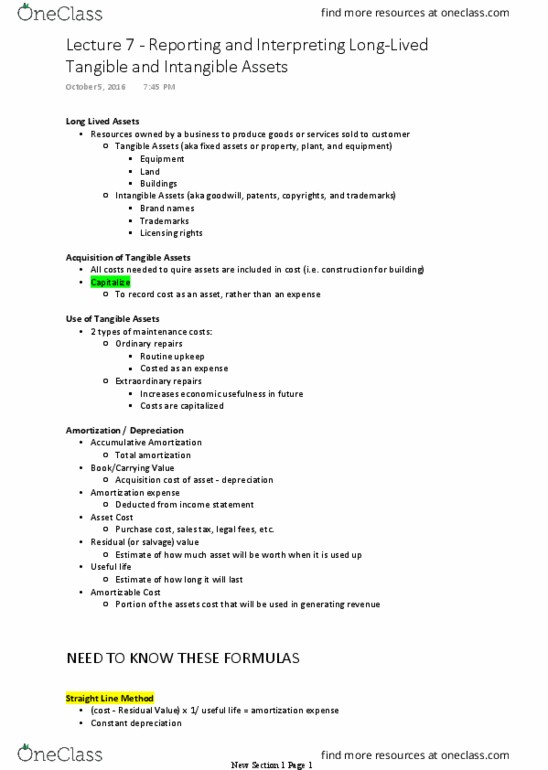

AFM123 Lecture Notes - Lecture 5: Canada Revenue Agency, 6 Years, Capital Asset

Document Summary

Get access

Related Documents

Related Questions

Produce a balance sheet for a company that distinguishes betweencurrent and non- current assets and liabilities.

Create a balance sheet from a trial balance.

Create a comparison of net income based on different methods ofinventory accounting.

Analyze a statement of cash flows and show where each line itemcan be found or

calculated from the other financial statements.

Prepare a full analysis of key financial ratios for a companyand state conclusions about

the financial strength of the company compared to industryratios.

PROJECT SUBMISSION PLAN

Project Part | Description/Requirements of Project Part | Evaluation Criteria |

1 | Title: Creating a Balance Sheet and Evaluating Inventory Task 1: Create a balance sheet from a trial balance for a givenscenario. Make sure you classify the accounts appropriately ascurrent or non-current. Click here to download the trialbalance. |

Page 1

AC1420: Project

Project Part | Description/Requirements of Project Part | Evaluation Criteria | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Task 2: Perform inventory valuations using LIFO, FIFO, andweighted average methods based on the following information.Explain the impact of each method on the cost of goods sold andending inventory. The company imports microwaves from a supplier in China for theUS market. At the end of the first quarter, 100 microwaves are instock. The company purchased a total of 400 microwaves during thequarter at various prices: January: 100 units @ $75 February: 250 units @ $83

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||