AFM121 Lecture 5: Topic 3 - 4

27 Dec 2015

School

Department

Course

Professor

Document Summary

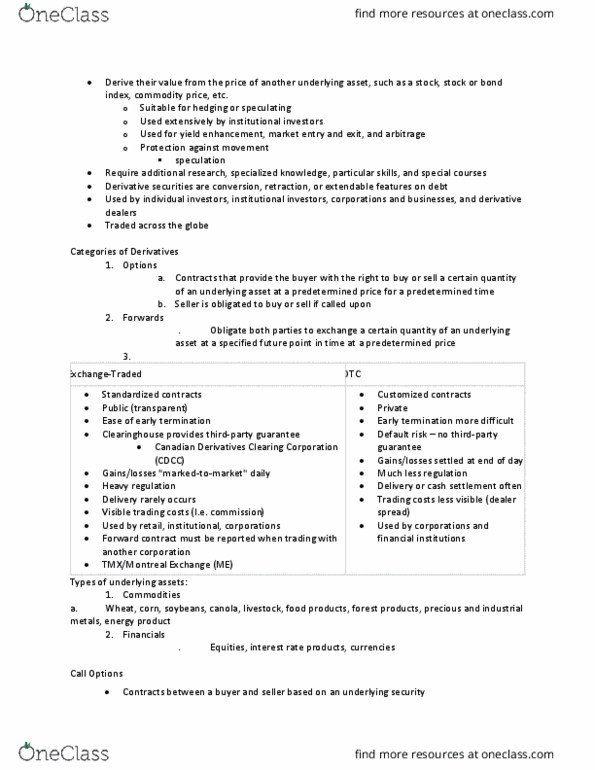

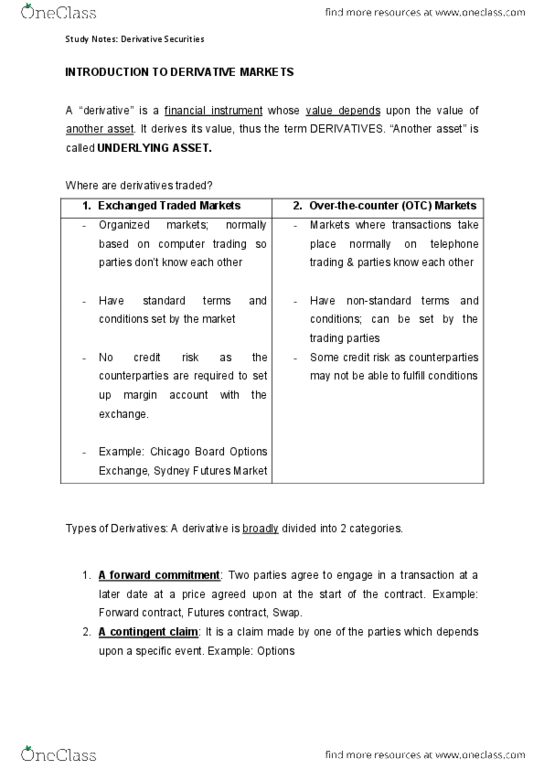

Futures securities the risk associated with this is a) the price of the asset at delivery date and b) the risk that the buyer will default. This contract starts with having no value, but its value grows over time as the prices change. Example: a ring maker makes an agreement to buy gold from a dealer at /oz. in 3 mo. The seller of the gold may be cautious about the risk and purchase the gold right now. If, now, along the line, the buyer decides not to buy, because the external prices available. He decides to cover his derivative position, as opposed to having a naked position. The riskiness of the deal (i. e. the return associated with an equally risky, forgone investment opportunity) = 6% Seller"s perspective costs, setting the price for the gold return. + incremental charges associated with holding the asset for the holding period (i. e. + storage + insurance) = 2%