ECON 1050 Lecture Notes - Lecture 6: Social Cost, Takers, Opportunity Cost

10 Nov 2018

School

Department

Course

Professor

Document Summary

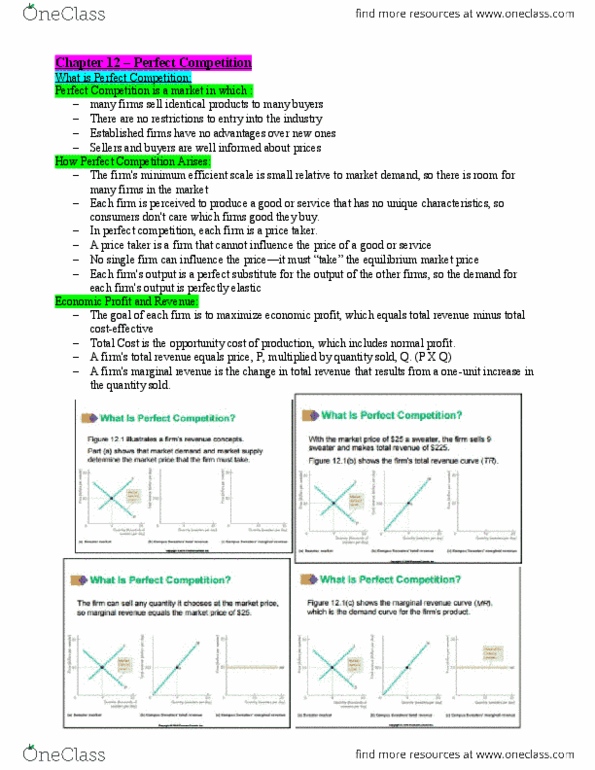

Perfect competition arises if the minimum efficient scale of a single product is small relative to the market demand for a good or service. Minimum efficient scale is the smallest output at which the lrac curve reaches its lowest output. In perfect competition, each firm produces a good with the sa(cid:373)e (cid:272)hara(cid:272)teristi(cid:272)s, so (cid:272)o(cid:374)su(cid:373)ers do(cid:374)"t (cid:272)are (cid:449)hi(cid:272)h fir(cid:373) the(cid:455) (cid:271)u(cid:455) fro(cid:373). A price taker is a firm that cannot influence the market price because its production is an insignificant part of the total market. Economic profit is equal to total revenue minus the total opportunity cost of production. Total revenue equals the price of a good or service multiplied by the quantity of the good or service sold. Marginal revenue is the change in total revenue that results from one more unit sold. In perfect competition, marginal revenue is equal to the market price.