RMIN 317 Lecture Notes - Lecture 2: Subrogation, Co-Insurance, Property Insurance

9 Dec 2017

School

Department

Course

Professor

Document Summary

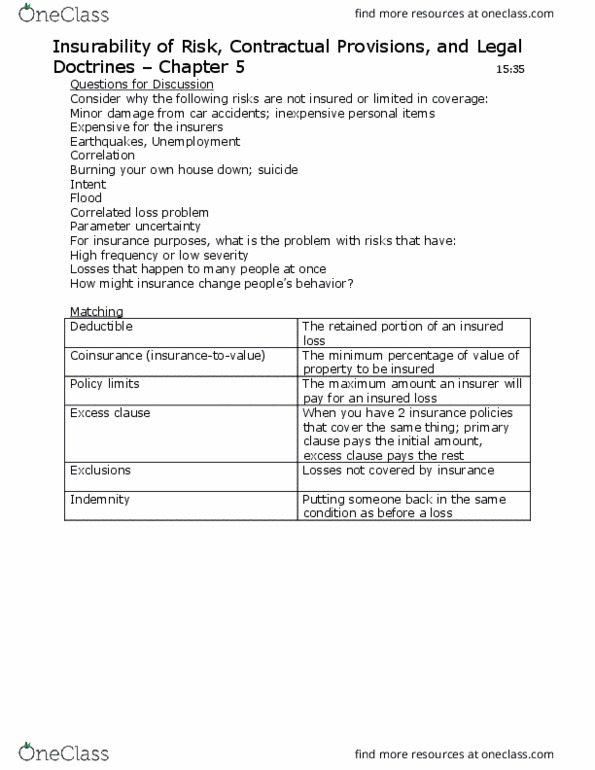

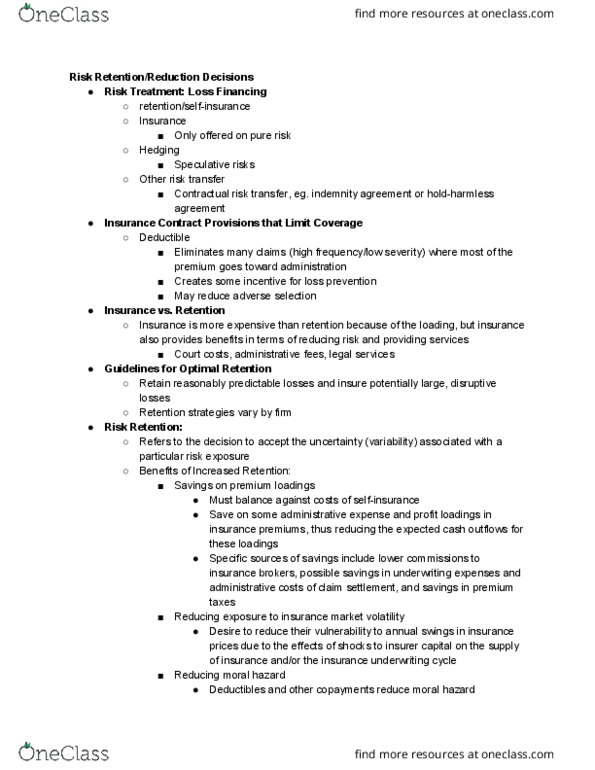

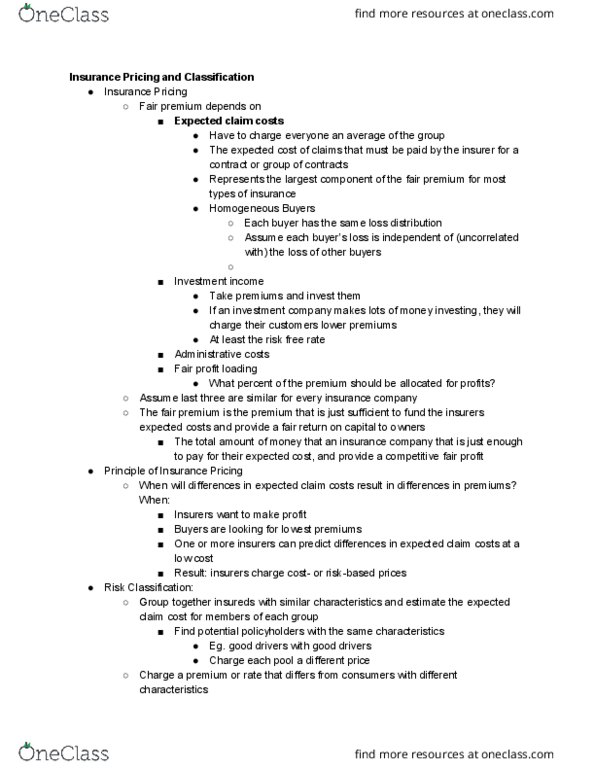

Insurability of risk, contractual provisions, and legal doctrines. Factors that limit the insurability of risk. If an insurance contract"s premium equals the present value of expected claims costs, a risk-averse person will likely demand full insurance coverage for monetary losses that otherwise would be paid by the person. Because premiums almost always have a positive loading, however, risk-averse people will demand less than full coverage. As the loading increases, the quantity of full coverage demanded is likely to decrease. Any factor that increases administrative or capital costs (and thus the loading on a policy) will limit the amount of private market insurance coverage. Higher premium loadings generally imply less coverage. Insurance coverage for some risk exposures is likely to be extremely limited or even nonexistent because of administrative and capital costs. Limited insurance coverage is more likely to occur for exposures with low severity, high frequency, correlated losses across people or businesses, and unknown loss distribution.