ACCTG311 Lecture Notes - Lecture 11: Cash Flow Statement, Deferral, Accounts Payable

16 Dec 2015

School

Department

Course

Professor

Document Summary

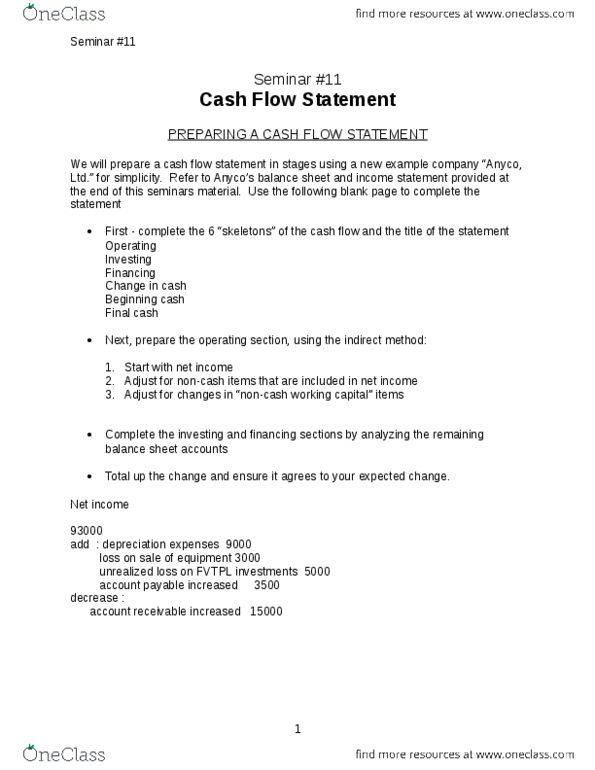

The equipment purchased with the bank loan is excluded. The assumption is that this was not cash in and then cash out, but rather a direct exchange (it isn"t the clearly presented here, but would be more clear in an exam). Cash flow is an important measure of return, compute the cash current debt and cash total debt coverage for 2015 and 2014 and interpret the results. (assume that cash from operations in 2014 was ,000. ) = cash prov. by operating activities / avg current liab. = cash prov by operating activities / avg total liab. Interpretation: the first ratio has improved slightly from the year before. This shows that anyco was able to generate cash in its day to day operations sufficient to cover its current liabilities. In 2015, anyco is generating cash flows from operations to cover its current liabilities by almost two fold.