BUS 320 Lecture Notes - Lecture 8: Financial Statement, Income Statement, Retained Earnings

3 Sep 2015

School

Department

Course

Professor

Document Summary

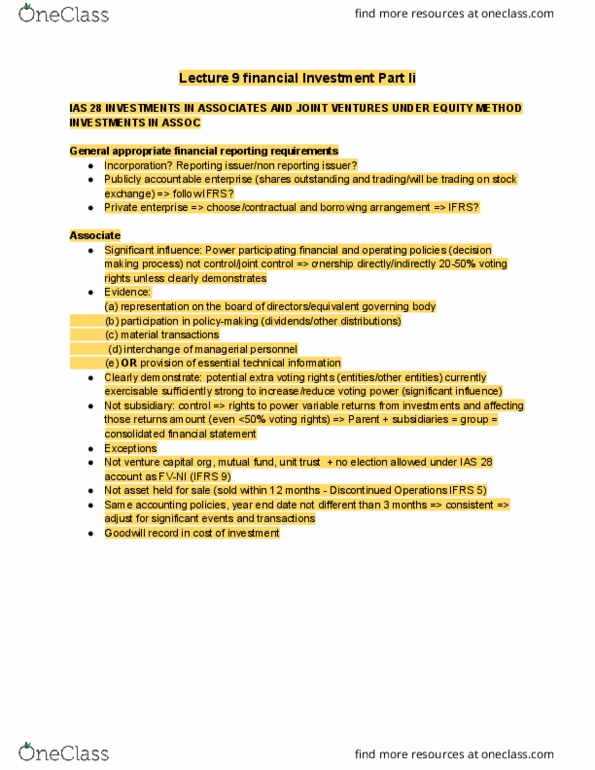

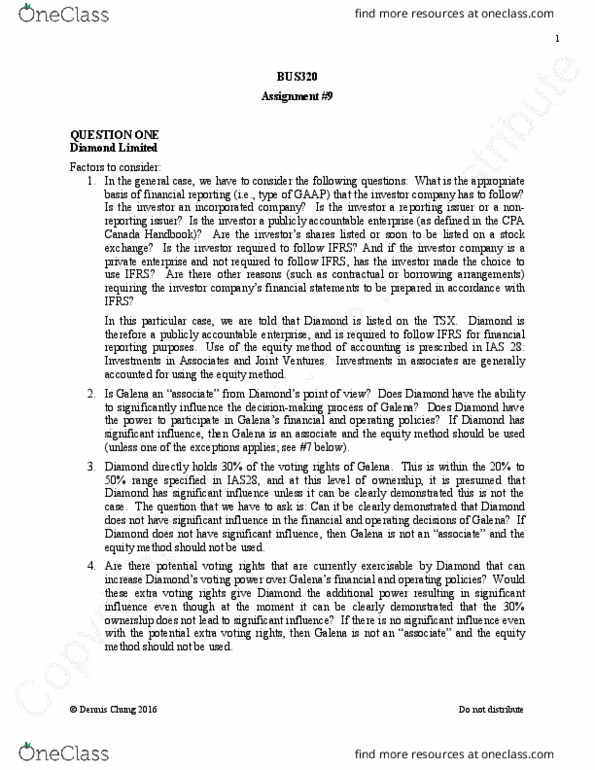

Buy into other companies to influence or control their activities. Involves the purchase of voting shares (common shares) in another company. Have an interest of less than 20: with little or no influence over the investee, maintain at fair market value. Buy to earn dividend revenue or to sell when profitable o. Have an interest of 20% to 50% o. Power to participate in the financial and operating policy decisions of an entity, but not control over those policies o o. Investment referred to as an associate (ias 38) Have an interest of greater than 50% o o o. Subsidiary company adds the following statements to its parent company. Record at cost (initially) and acquisition expenses (after) of acquired shares. Recognize investment income as the investee earns income. Treat investment as part of company by o o. Increasing investment account by share of earnings of the associate.