BUS 320 Lecture Notes - Lecture 7: Ias 39, Cash Flow, Book Value

3 Sep 2015

School

Department

Course

Professor

Document Summary

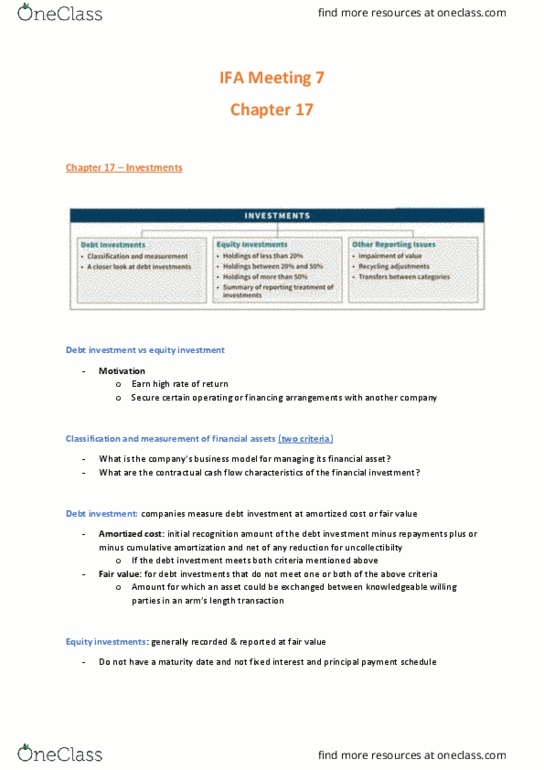

Reasons for holding investments: earn return on idle cash o o o. Easily sold: when cash is needed or price is right. Usually pay interest, dividends, and cash equivalents: develop a portfolio of investments. Sell when price changes or hold to maturity. Earn interest or dividends o o o o. Invest for strategic reasons o o o o. Buy into other companies to influence or control their activities. Usually equity investment as debt does not provide much leverage. Basis of classification (ifrs 9) o o. The company"s business model for managing the financial assets. The contractual cash flow characteristic of the financial asset. Investments with fixed payments of principal and interest. Applies to investments in debt securities and long-term note and loans receivable. Recognize the cost of investment at fair value of the debt acquired. Premium or discount is amortized over the life of the asset. No gain/loss at maturity date because cash is received o.