BUS 315 Lecture Notes - Lecture 7: Risk Measure, Sharpe Ratio, Standard Deviation

19 Jun 2016

School

Department

Course

Professor

Document Summary

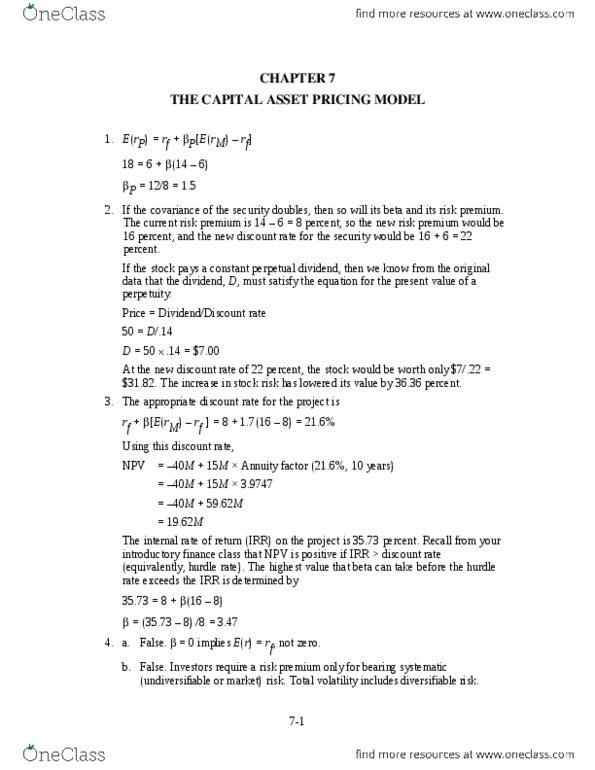

If the covariance of the security doubles, then so will its beta and its risk premium. The current risk premium is 14 6 = 8 percent, so the new risk premium would be. 16 percent, and the new discount rate for the security would be 16 + 6 = 22 percent. If the stock pays a constant perpetual dividend, then we know from the original data that the dividend, d, must satisfy the equation for the present value of a perpetuity: At the new discount rate of 22 percent, the stock would be worth only /. 22 = The increase in stock risk has lowered its value by 36. 36 percent. The appropriate discount rate for the project is rf + [e(rm) rf ] = 8 + 1. 7(16 8) = 21. 6% Npv = 40m + 15m annuity factor (21. 6%, 10 years) The internal rate of return (irr) on the project is 35. 73 percent.